Background

ESG has officially entered the mid-market boardroom. Sustainability sections now feature prominently in annual reports. Mid-sized companies display framework badges with pride such as GRI, TCFD, and SASB, and fill pages with metrics, values, and diagrams tracing their impact across the value chain.

What many mid-sized firms have built however, is ESG optics, not ESG integration. ESG continues to largely operate as a standalone disclosure compliance driven function, decoupled from Enterprise Risk Management (ERM), and operational decision making.

The cost of this structural disconnect is rising. Investors are demanding alignment between ESG strategy and business outcomes. Operational incidents are increasingly linked to blind spots that ESG frameworks were supposed to surface but didn’t.

This article examines the widening gap between ESG reporting and ESG risk integration in mid-sized firms. When it refers to ESG risks, it points to a broad but tangible spectrum of exposures. These include climate transition shocks, biodiversity loss, labour rights violations, greenwashing, data breaches, supply chain vulnerabilities, and governance failures. These are not theoretical risks. They show up as project delays, litigation, regulatory penalties, capital constraints, and reputational damage. For mid-sized firms, exposure is growing, but the ability to anticipate, measure, and mitigate ESG risks often falls short. This article explores that disconnect and lays out a blueprint for embedding ESG into the core of ERM, where it belongs.

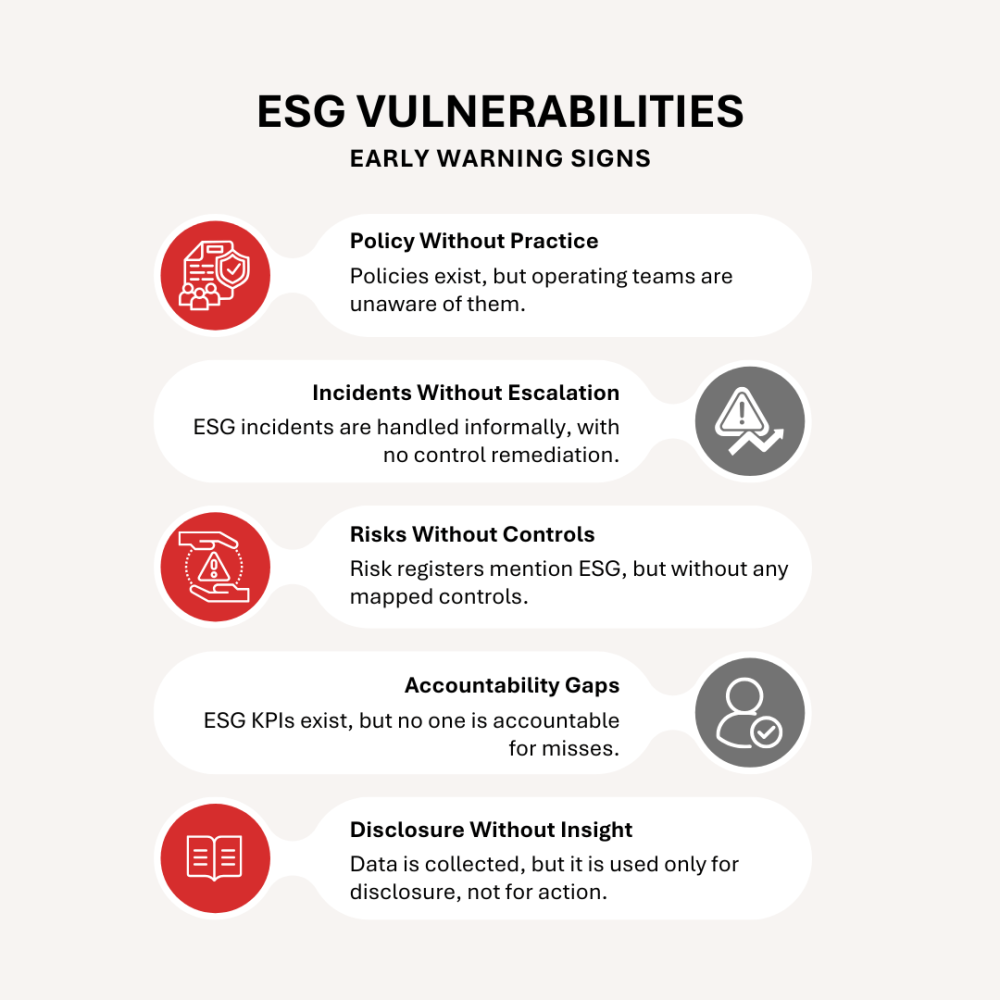

Where Integration Breaks: Key Vulnerabilities

a. Scattered Ownership, Hollow Oversight

- This diffusion is often a legacy of how ESG has evolved in resource constrained settings. Without dedicated teams, ESG has tended to land where bandwidth exists at a point in time, not where strategic alignment lies.

- Ask who is accountable, and the answers are often unclear or contradictory. CSR may manage community initiatives, risk taking on climate, legal handling disclosures, and HR overseeing diversity. Responsibilities are thus scatteredwith little coordination between units.

- When issues emerge, responses are disjointed. A vendor may face human rights violations or a site may breach environmental norms, but coordination falters. In such moments, governance gaps surface.

- The result is symbolic oversight where updates are shared, dashboards reviewed, but material risks go unchallenged. What looks like oversight proves to be a reporting theatre. ESG exists, but it does not lead.

b. Disconnection from Enterprise Risk Management (ERM)

- Scan a typical risk register of a mid-sized company and you will likely find familiar entries: operational, credit, cyber, reputational or regulatory risks. But sustainability exposures such as water scarcity, human rights violations, or climate transition risk areoften missing. This omission reflects a deeper structural misalignment. ESG risks are not just underreported, they are mismanaged.A major Indian outsourcing firm was recently embroiled in controversy after labour and data protection lapses surfaced. Global clients were drawn into the cross-border implications, revealing how ESG vulnerabilities within third-party ecosystems can escalate into legal, operational, and reputational crises when not integrated into enterprise risk frameworks.

- ESG and risk teams usually operate on separate tracks, guided by different templates, language, and reporting cycles. There is limited dialogue, shared metrics, and few common touchpoints in governance. The consequences are tangible. Risks that are not integrated do not get assessed, tracked, or mitigated.

- Decisions on capital deployment, supplier onboarding, or market entry move forward without proper accounting of ESG exposure. And when ESG risks crystallize, whether through forced labour allegations or carbon price shocks, they hit as surprises, not scenarios planned for. The fallout is reputational, financial, and at times regulatory.

c. Short-Term Fixes, Long-Term Blind Spots

- ESG risk management in many mid-sized firms still remains reactive. Environmental near misses, whistleblower alerts, or supplier violations are resolved in isolation. They are treated as incidents to close, not signals of operational risk.

- These events rarely trigger cross-functional reviews or governance reform. They are often viewed through conventional lenses like outsourcing, reputational, or compliance risk, rather than as ESG issues warranting systemic attention.

- Most incident platforms are not equipped to tag and escalate ESG-related risks across risk taxonomies or internal audit programs. As a result, these incidents are captured but not translated into lasting controls or reforms. ESG concerns remain excluded from the formal risk universe, leaving gaps in ownership, escalation, and consequence management.

- The problem is not that patterns go unnoticed. It is that they are seen, logged, and filed away without institutional learning. With no feedback loop between ESG events and core GRC systems, the organisation remains in a state of incident-by-incident reaction. The absence of structural course correction keeps ESG risk in the background, never part of the firm’s control spine.

d. ESG as Policy, not Practice

- Many mid-sized firms have made substaintial progress in formalising ESG commitments, issuing environmental policies, supplier codes of conduct, and diversity statements. On paper, the structure appears sound but in practice, ESG often remains disconnected from core governance and risk processes.

- In GRC terms, ESG policies are frequently documented but not operationalised. They may not inform procurement thresholds, risk assessments, or investment decisions. First and second-line functions often lack clarity on ownership, escalation, or how ESG ties into day-to-day decision-making. Without mapped controls, training protocols, and integration into assurance cycles, these policies function more as signals of intent than tools of control.

- Compouding the complexity is proliferation of various frameworks leading to disclosure misalignment. Many organizations struggle to reconcile overlapping or divergent expectations, resulting in fragmented reporting and diluted strategic focus.

- This gap is not always a result of indifference. Competing compliance pressures and resource constraints can slow down implementation. Without intentional follow-through, even the most well-designed policies fall short of delivering meaningful risk mitigation. ESG maturity must be measured not by the presence of documents, but by the presence of systems that activate them when it matters.

e. When ESG Goals and Rewards Don’t Align

- In many mid-sized firms, ESG targets exist on paper but lack execution in practice. Sustainability teams may be commended for reporting achievements, yet the broader organization remains focused on financial KPIs that often conflict with ESG goals. Cost pressures get passed down the value chain leading to corner-cutting, while accelerated timelines increase the likelihood of environmental or safety incidents.

- A key barrier is the weak integration of ESG into performance architecture. Where ESG metrics appear in bonus scorecards, they are often peripheral, vaguely defined, or outweighed by short-term financial goals. This imbalance is particularly visible at senior levels, where ESG objectives are seldom treated with the same urgency as revenue or margin targets.

- The result is a misalignment between declared priorities and actual behaviour. Employees learn to focus on what is measured and rewarded. When ESG is not embedded in those levers, it struggles to influence decisions in a meaningful way, not because intent is lacking, but because the system is not built to support it.

f. Over-indexing on Reporting Tools, Underinvesting in Control Maturity

- Across the mid-market, ESG dashboards and disclosure software are on the rise. Companies invest in sleek platforms that automate surveys, generate visual reports, and populate sustainability portals with curated metrics. Even though ESG data may feed disclosure reports, but it often bypasses the systems that govern enterprise control like incident management, RCSA, and third-party audits. The result is a disconnect where core risk systems remain unchanged, limiting the shift from insight to action.

- Compounding this issue is the poor quality of ESG data generated by many reporting systems. Inconsistent methodologies, unverifiable metrics, and outdated sources often result in low-confidence inputs. When such flawed data becomes the basis for business decisions, it not only undermines credibility but exposes firms to material risk misjudgments.

- A large European asset manager came under investigation in 2022 after national regulators launched a raid based on allegations of greenwashing. Although its ESG disclosures were extensive, internal records and control reviews indicated that several funds were marketed as ESG aligned without sufficient substantiation. The optics of compliance had obscured the absence of effective governance. The result was regulatory backlash, investor exits, and significant reputational damage.

- The more firms over index on optics without reinforcing the control layer beneath, the more exposed they become to ESG failures, reputational damage, and regulatory sanctions that reporting alone cannot defend against.

- Bridging the ESG gap requires more than software fixes or better disclosures. It calls for a reset in how companies assign ownership, integrate ESG into risk frameworks, and translate accountability into daily decisions. The blueprint that follows outlines practical steps mid-sized firms can take to move ESG from narrative to control reality, one that holds up under scrutiny and improves performance from the inside out.

Embedding ESG within ERM Framework – A blueprint

a. Governance & Strategy

- Clarify ESG Ownership: Assign ESG accountability at the board and CxO levels. Establish cross-functional steering committees that include leaders from risk, operations, sustainability, legal, and procurement. Make roles explicit. When responsibility is shared without clarity, it leads to inaction.

- Link ESG KPIs to Leadership Appraisals: Incorporate progress on ESG metrics into formal executive performance reviews. Tie variable compensation to tangible ESG outcomes, not just the completion of disclosure requirements.

- Scrutinize ESG Trade Offs: Institutionalize ESG risk and benefit analysis in capital allocation, procurement, and growth decisions. All major investments should be assessed for ESG exposure by the relevant committees before approval.

- Align with Risk Appetite and Code of Conduct: Embed ESG criteria within the organization’s stated risk appetite. Clearly define what levels of trade off between short term gains and long term risks to reputation, compliance, or sustainability are acceptable and what are not.

b. Risk Integration & Controls

- Embed ESG in a Risk Based Framework: Integrate ESG into enterprise-wide risk identification, assessment, and escalation processes. Focus on what is material and purpose driven, ensuring ESG risks are treated with the same discipline as financial or operational exposures.

- Expand the Risk Taxonomy and Assign Ownership: Update enterprise risk taxonomies to include exposures such as climate disruption, labour rights, data governance, and supply chain integrity. Ensure every function maps its relevant ESG risks into the central register with defined controls, owners, and mitigation plans.

- Establish ESG-Linked Key Risk Indicators: Monitor leading signals such as supplier code violations, whistleblower reports, or environmental breaches. Set thresholds that trigger escalation through existing governance channels to avoid fragmented oversight.

c. People & Accountability

- Build Practical ESG Fluency Across Functions: Move beyond theoretical training. Equip operations, finance, procurement, and HR teams with role-specific ESG guidance that informs day-to-day decisions, trade offs, and escalation procedures.

- Distribute Responsibility Across the Front Line: ESG ownership should not rest solely with sustainability or reporting teams. Link ESG responsibilities to operational roles, with measurable targets tied to control implementation, risk mitigation, and incident reporting.

- Enforce Structured Escalation for ESG Breaches: Treat ESG failures with the same urgency as financial or operational breakdowns. Supplier violations, environmental incidents, or workplace grievances must trigger a formal response, including remediation steps and governance review.

d. Data, Reporting & Technology

- Integrate ESG into Risk and Control Systems: Move ESG from static reports to live data streams embedded in incident management tools, RCSA processes, and third party risk platforms. Ensure ESG risks and breaches inform how the organisation governs and responds in real time.

- Design ESG Data for Actionability: Prioritise usability over volume. Enable procurement teams to flag supplier risks, operations to monitor environmental exposure, and risk committees to evaluate trade offs. Insight, not collection, is the objective.

- Test Control Implementation, Not Just Documentation: Go beyond policy checklists. Monitor if ESG controls are actually followed, assess how they perform under pressure, and use internal audits to uncover weak links and emerging issues.

- Use Technology to Scale Discipline, Not Bypass It: Leverage tools to centralise ESG data, trigger alerts, and map exposure. Technology should support control ownership and follow through, not replace it.

Care should be take however when introducing ESG scoring systems powered by AI. When underlying data or algorithms carry historical bias, AI tools can amplify discrimination, skew assessments. Organizations must exercise caution and ensure AI tools are explainable, monitored, and contextually validated.

Conclusion – Transitioning From Blueprint to Benchmark

Embedding ESG into GRC needs more than intent. It requires ongoing assessment. The indicators below offer a practical way to evaluate how ESG risk is being integrated across key decision-making processes. They reflect whether ESG is influencing governance, operations, and risk management in a consistent and structured manner.

These metrics go beyond compliance. When used thoughtfully, they provide insight into how ESG is shaping internal behaviours, influencing leadership decisions, and guiding procurement and oversight. Tracking trends across these indicators can help firms identify where integration is working and where it needs reinforcement.

External certifications can play a supporting role, provided they are used to validate embedded practices rather than serve as stand-ins for them. When done right, they help demonstrate that ESG is being taken seriously in practice, not just on paper.

For mid-sized companies at the ESG inflection point, the question is no longer about ticking the disclosure box. It is about control. True resilience comes from whether ESG risks are embedded into governance, operational controls, and decision-making frameworks.

This is a structural shift requiring clear ownership, alignment with enterprise risk, and readiness to adapt. Real resilience comes from how ESG informs how a company governs itself, manages risk, and drives accountability.

The real shift lies in moving from “Are we ESG-compliant?” to “Is ESG risk embedded in the way we govern, decide, and operate?”

Leave a Reply