Welcome to the inaugural episode of Karmine Kompass: Pivotal Conversations!

We kick off our journey to excellence with Shreyas Tonse of Zensible, the world’s first Total Experience (Tx) company in HR technology. This conversation is your roadmap to understanding the strategic shift needed to succeed in the digital-first era.

We dive deep into why enterprises need to stop viewing HR software as fragmented tools and start treating it as a unified, strategic ecosystem that maximizes business value and employee experience.

Karmine Consulting is dedicated to guiding leaders through pivotal conversations. Subscribe for weekly insights that inspire, ignite, and align your business strategy.

For some time now, the “money mule” typologies have largely involved vulnerable individuals who were persuaded or coerced into moving illicit funds. Today, that typology is shifting into exploiting legitimate business current accounts, especially those belonging to MSMEs, to layer and route illicit funds at scale. This evolution is not just tactical; rather, it represents a well thought out reconfiguration of how criminal networks exploit the trust fabric underpinning the financial system.

Recent cases reported across Indian banks highlight how MSME accounts are being hijacked, rented, or compromised to facilitate fast-moving, high-velocity transfers. This trend is accelerating, and financial institutions must re-evaluate their fraud detection and prevention strategies before systemic trust erodes any further.

Business Accounts – New Mule Infrastructure

1. Higher Transaction Thresholds

Business current accounts routinely handle large-value transactions. A ₹3-5 lakh credit in an MSME account appears routine, whereas the same amount would seem anomalous in a retail account. This gives fraudsters a degree of anonymity through normalcy.

2. Legitimacy and Established History

Contrary to newly opened personal bank accounts, corporate entities generally come with a certain level of banking history, GST filings, payroll patterns, and vendor relationships. This legitimacy provides the necessary camouflage for fraudsters to move funds through current accounts.

Often attributed as “Rent-a-Current-Account” model, struggling businesses, especially those with credit stress, rent their accounts for commissions where funds are layered through vendors, wallets, and forex channels before exiting the system.

3. Lower Behavioural Predictability

MSME activities differ dramatically across sectors based on their seasonality, client mixes, and growth cycles. This diversity makes it difficult for traditional transaction monitoring systems to establish a baseline for what “good” account behavior looks like.

4. Insider or Peripheral Collusion

Fraudsters capitalize on dormant partners, distressed business owners, accountants, or even compromised vendor relationships. In other cases, attackers gain access through identity compromise, or invoice-manipulation attacks.

Criminal networks now favor “fewer, high-trust mule accounts” over a network of small retail mules, allowing them to transfer larger volumes with reduced exposure.

5. Account Takeover via Business Email Compromise

Cybercriminals compromise corporate email systems, intercept invoices, alter payment instructions, and quietly redirect funds into compromised or rented business accounts.

6. Shell Firms Masquerading as Genuine MSMEs

Criminals create fully documented shell companies, complete with incorporation proofs, basic trade activity, and GST registrations, to simulate legitimacy while acting as laundering pipelines.

The common thread across all three is the exploitation of blind spots within traditional bank surveillance and due diligence procedures.

Why Traditional Controls Fail

1. Static KYC cannot keep up with dynamic risk

KYC establishes identity at the time of onboarding or during periodic refresh, but businesses often evolve faster than the KYC cycle, sometimes into riskier entities. Without dynamic risk-refresh mechanisms or perpetual KYC procedures, banks remain blind to behavioural drift.

2. Typical transaction monitoring typologies not designed for MSME complexity

Rule-based transaction monitoring engines falter with MSMEs whose cash flows are non-linear, seasonal, and shaped by sector dynamics. As a result, generic rules either flood systems with false positives or miss detecting targeted mule activity.

3. Lack of entity-resolution across accounts & identities

A business is not a single account, rather it is an ecosystem of promoters, directors, accountants, devices, IPs, and counterparties. Legacy systems struggle to connect these signals and form a unified risk picture, analyzing each data point in isolation which creates blind spots that delay detection and prevents banks from recognizing coordinated or evolving threats across the wider business ecosystem.

4. Limited Visibility Beyond the Bank’s Perimeter

Fraud patterns often spread across institutions, but without consortium-level intelligence or federated learning programs, these signals stay under the radar. Fraudsters take advantage of this fragmentation, moving quickly between institutions to stay ahead of detection.

Building Models that work – Our Perspective

The surge in business-account mule activity highlights a crucial industry lesson: fraud cannot be solved through transaction monitoring alone. Detecting mule behavior, particularly in corporate accounts, requires multi-dimensional intelligence that connects digital signals, human context, and behavioural narratives.

Karmine’s perspective centers on four essential pillars.

A robust Customer 360° framework brings together identity, device, and behavioural signals across both retail and corporate profiles and integrates fraud and AML so that indicators such as account-takeover attempts or suspicious logins strengthen AML risk scoring. It also incorporates network-level intelligence to reveal links to shell firms, risky beneficiaries, or high-velocity counterparty rings.

Traditional systems often treat fraud and AML as separate domains, even though mule activity sits directly at their intersection. A single, entity-level view can uncover risk patterns that often get missed in siloed systems.

Only when a bank views the business as a single, holistic entity, rather than as a collection of accounts, can mule activity be detected in time.

2. Early Risk Signals Appear Long Before Transactions Do

Documentation inconsistencies, KYB anomalies, and behavioural red flags often emerge months before any transactional anomalies surface. These early signals provide valuable insight into whether a business is stable, legitimate, and operating as declared.

Examples include mismatches between the stated nature of business and actual financial flows, templated or recycled incorporation documents, unexplained changes in ownership or authorized signatories, and income lines or operational footprints that do not match the speed of fund inflows. These indicators often hold predictive value and can highlight elevated risk before money movement becomes suspicious.

To use this intelligence effectively, banks must integrate these non-transactional signals into their ongoing monitoring processes. When onboarding and KYB data is treated as one-time paperwork instead of continuous risk input, institutions lose early warning capabilities that can prevent misuse long before transactional behavior deteriorates.

3. Relationship Managers – crucial interpreters of customer behavior

For corporate and MSME segments, Relationship Managers (RMs) are a primary source of contextual understanding. They know their clients’ operational realities, seasonality, and market cycles, yet in most banks the RM layer remains disconnected from fraud and AML signals.

To be effective, RMs need the ability to spot deviations between expected business behavior and actual transaction flows, escalate sudden shifts in volume, beneficiaries, or geographies, and validate whether a company’s banking behavior aligns with the patterns observed. Digital intelligence can detect anomalies, but only human context can explain them.

4. Strong, Continuous KYC/KYB – A Non-Negotiable

The shift from a legitimate business to a mule entity is often gradual, which makes static KYC frameworks insufficient on their own. A more continuous, risk-based KYB approach is needed, where updates are prompted by behavioural changes rather than waiting for a scheduled refresh.

In practice, this means keeping an eye on sector-specific cash-flow patterns, checking whether the business model still appears viable, and periodically validating key details such as income sources, counterparties, staffing, and day-to-day operations. Simple, contextual risk scoring can help highlight when a business begins to deviate from its usual activity. In this model, understanding how a business operates becomes just as important as confirming who owns it.

How Karmine Consulting can help

For banks dealing with MSME portfolios, the real challenge is not just detecting mule accounts but understanding where and why the current system is blind. As a boutique AFC consulting firm, we aid institutions across some of their core considerations:

Governance & Risk Profile: Build a sharper, enterprise-level view of their MSME mule risk profile by identifying which sectors, clusters, ownership patterns, and transaction behaviors create the highest exposure.

Data: We aid in mapping data landscape end-to-end, assessing where relevant signals sit across KYC, GST data, account behaviors, trade documents, RM logs and counterparty flows and how much of this can be orchestrated to strengthen detection without waiting for multi-year modernization.

Process: We help refine processes for faster identification and cleaner reporting, redesign accountability structures across the three lines of defense, and define the RM/analyst skill sets needed to distinguish legitimate MSME churn from mule activity.

Tech: Finally, we help banks pinpoint the exact tech investments that will move the needle across entity resolution, network-graph analytics, document forensics, or continuous-KYC triggers.

Through our interventions, we help ensure institutions build a scalable, intelligence-led MSME mule-detection capability rather than repurposing retail-focused controls

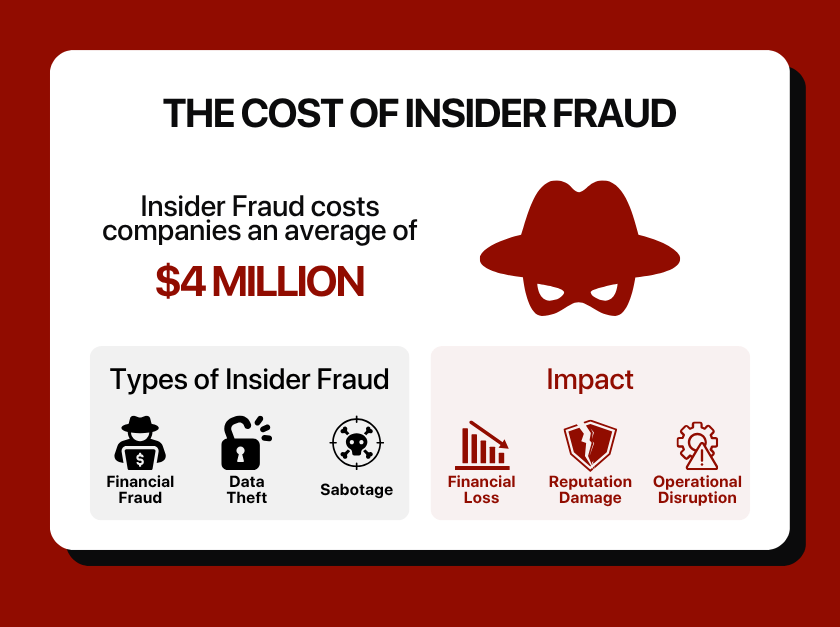

When it comes to risk management, mid-sized listed companies often focus on external threats—cyberattacks, market volatility, regulatory changes. Yet, one of the most damaging risks can come from within: insider risk, where employees or trusted parties collude to commit fraud.

Insiders are behind a significant share of corporate fraud and data breaches, costing businesses millions. A recent global study by the Association of Certified Fraud Examiners (ACFE) found that organizations typically lose 5% of their annual revenue to occupational fraud (which by definition involves insiders), with total losses exceeding$3 billion in the cases studied. The median loss per internal fraud case was$145,000—a hefty hit for a mid-sized firm. Losses as a percentage of revenue tend to be higher in smaller organizations than in large enterprises.

In short, the threat from within can be as damaging as any external attack, yet it doesn’t always get the attention it deserves.

Defining the Insider Threat Spectrum

Insider threats span a spectrum of behaviors—malicious, conflicted, fraudulent, or negligent—each with distinct triggers and impacts. Understanding these typologies is essential for proactive risk management.

Malicious Insiders

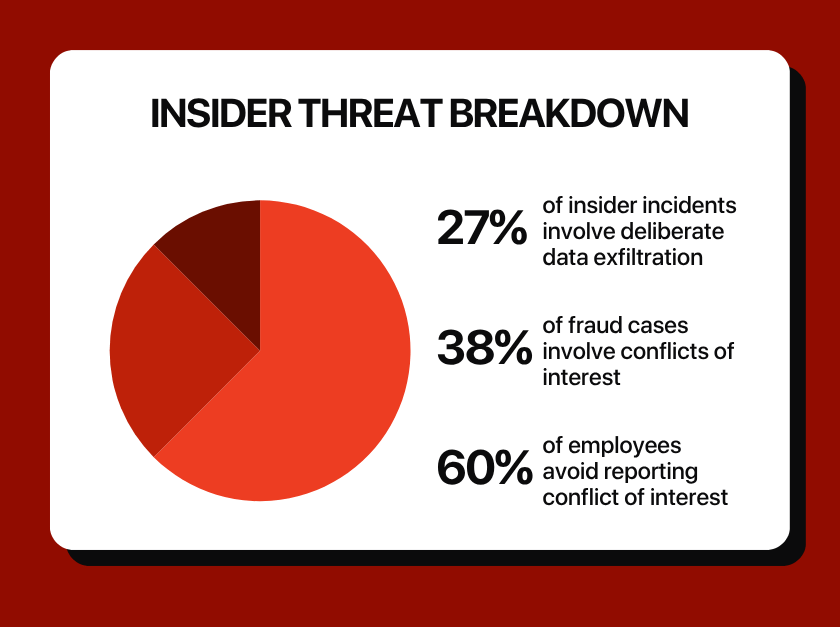

Malicious insiders intentionally harm the organization through actions like data theft or sabotage. Triggers include financial distress, disgruntlement, or external coercion. For example, an IT administrator at a mid-cap tech firm might leak customer data to a competitor for financial gain, exploiting elevated access privileges. The 2025 Ponemon Institute report noted that 27% of insider incidents involve deliberate data exfiltration, costing$15.3 million on average.

Conflicted Insiders

Conflicted insiders prioritize personal gain through undisclosed vendor ties or related-party deals. Triggers include personal relationships or financial incentives. A 2023 EY Fraud Survey found 38% of fraud cases in mid-caps involve conflicts of interest, such as a procurement officer awarding contracts to a relative’s firm without disclosure. Weak oversight exacerbates these risks, as mid-caps often lack automated vendor screening.

Silent Fraud

Silent fraud involves subtle misconduct, such as skimming, expense misreporting, or privilege abuse, often enabled by weak controls. For instance, an employee inflating expense reports might go undetected without automated reconciliation, draining resources over time.

Negligent Insiders

Negligent insiders cause harm through human error or poor control hygiene, such as clicking phishing links or mishandling sensitive data. For example, an employee downloading malware via an unverified link could expose customer data, leading to costly breaches.

Third-Party Threats

Contractors or vendors who have inside access can compromise security, either intentionally or via lax practices.

Why Growing Companies Are Especially Vulnerable

Growing companies are often large enough to present ample opportunities for internal fraud, but they may not yet have the robust controls and corporate governance that mature enterprises deploy. Rapid growth can strain internal processes. New departments, higher transaction volumes, and more employees may outpace the development of a strong control environment.

Informal Trust Culture

Tight-knit teams often prioritize harmony over scrutiny. Employees hesitate to report colleagues, fearing conflict or disruption. Without formal escalation channels, early red flags go unnoticed. A study found 60% of employees avoid reporting conflicts of interest to preserve team dynamics, underscoring how silence becomes the norm in trust-heavy environments.

Limited GRC Resources and Budget Constraints

Most mid-sized companies operate with lean GRC teams. Budget constraints hinder investment in fraud detection tools like user behavior analytics or real-time alert systems. According to ACFE’s 2024 study, over half of all fraud cases occur due to weak or overridden internal controls—a risk magnified in firms lacking dedicated compliance capacity.Most mid-sized companies operate with lean GRC teams. Budget constraints hinder investment in fraud detection tools like user behavior analytics or real-time alert systems. According to ACFE’s 2024 study, over half of all fraud cases occur due to weak or overridden internal controls—a risk magnified in firms lacking dedicated compliance capacity.

Blind Trust in Long-Serving Employees

Familiarity breeds complacency. Many insider incidents involve staff considered loyal or beyond suspicion. The Ponemon Institute found that 1 in 5 insider frauds involved “trusted” employees exploiting privileged access. When firms equate tenure with integrity, they often ignore the need for independent oversight or segregation of duties, leaving room for misconduct.

Compliance Gaps in Listed Mid-Caps

Being publicly listed doesn’t guarantee governance maturity. Many mid-cap firms face regulatory obligations without scaled internal systems to meet them. A 2024 survey showed 55% of listed mid-sized firms lacked robust compliance frameworks, increasing exposure to fraud, conflicts of interest, and enforcement risks.

Neglect of Insider Behavior Monitoring

While external threats like cyberattacks, audits, and investor scrutiny often dominate risk discussions, internal behavior in mid-sized firms remains largely unmonitored. A 2024 report found that while insiders were involved in 60% of data breaches, only 25% of companies regularly monitor user activity. This oversight gap allows repeated privilege abuse or policy violations to slip through undetected.

Cultural Resistance to Monitoring Tools

Employee pushback is common when firms try to implement tracking tools. In trust-driven environments, monitoring feels intrusive and misaligned with the culture. A recent survey revealed that 63% of employees would consider leaving their company if strict monitoring measures were put in place. This resistance slows adoption of essential controls like access logging or behavioral alerts.

Overlapping Roles and Conflicts of Interest

In mid-sized setups, employees often wear multiple hats, including approving vendors, processing payments, and handling reconciliations. This lack of segregation weakens internal checks. ACFE reports that 42% of frauds stem from the absence or override of internal controls, such as dual approval or independent reviews.

Manual Workflows and Silent Fraud

Email-based processes, spreadsheet approvals, and informal reimbursements create room for “quiet” fraud. Without automated alerts or audit trails, misconduct can persist unnoticed. A 2025 Bloomberg case revealed how a mid-sized retailer lost$1.8 million over two years through undetected expense fraud, highlighting the cost of informal systems.

Regulatory Burden Without Execution Support

Compliance demands are growing, but mid-sized firms often lack the structure to execute. From data protection to ESG, obligations now rival those of large enterprises, without matching resources. The U.S. Chamber of Commerce noted in 2024 that 51% of small and mid-sized businesses see regulation as a key operational burden.

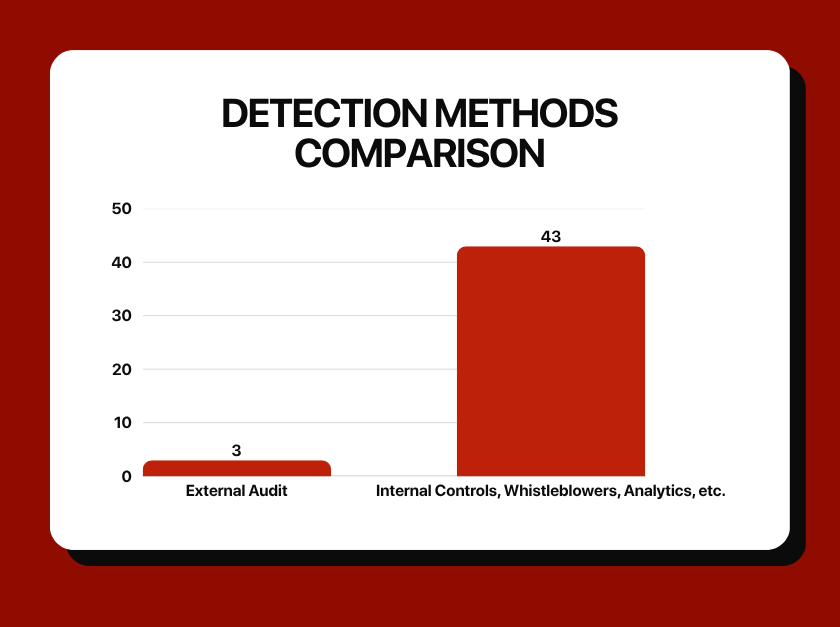

Overreliance on Financial Audits

Annual audits offer false comfort. ACFE data shows external auditors detect only 3% of fraud cases. Behavioral misconduct like override abuse or insider collusion rarely shows up in financial statements. Without internal controls focused on behavior, red flags remain buried in day-to-day operations.

Mitigating Insider Risk

Mid-sized firms often walk a tightrope between agility and oversight. With lean GRC teams, fast-moving operations, and high dependence on trust, insider risk becomes a quiet but potent threat, often surfacing only after the damage is done. Fortunately, leading companies are showing how risk exposure can be materially reduced through deliberate, scalable steps:

Build Professional Skepticism Across Vulnerable Functions The absence of healthy doubt is a core enabler of internal fraud. Teams often trust colleagues or assume “it must have been reviewed.” Embedding professional skepticism via training, risk orientation, and scenario-based workshops can shift the mindset from “compliance” to “risk management.” For example, a Southeast Asian mid-cap embedded a red-flag checklist in monthly reviews, flagging odd vendor payment cycles, duplicate invoices, and large round-number payments, unearthing a 3-year-old ghost vendor scheme.

Layer Forensic Thinking Into Control Design Traditional controls (approvals, reconciliations) often lack the forensic intent to catch manipulation. Mid-sized firms should embed anti-fraud thinking into finance and procurement workflows, e.g., flagging new vendors created by the same user who approves invoices, or detecting payment splits just below approval thresholds. In one Indian mid-cap, forensic review of vendor master data found multiple entries linked to a single PAN number, leading to the unravelling of a procurement kickback loop.

Regular Rotation of Duties in Sensitive Functions Fraud schemes often rely on a single insider managing a process end-to-end. Periodic job rotations, especially in roles like vendor onboarding, payroll processing, or loan disbursements, introduce fresh eyes and reduce opportunity. This approach helped a fintech firm in India detect a backdated disbursement manipulation after a temporary replacement questioned an old approval trail.

Maintain an Always-On Fraud Ledger Beyond incident response, firms should maintain a fraud event registry tracking red flags, near misses, overrides, and ethical hotline tips, even if they don’t lead to confirmed fraud. Patterns often emerge when seen over time. One APAC manufacturer built such a ledger, which helped internal audit connect repeated override incidents across multiple geographies, ultimately leading to the identification of a multi-country expense fraud ring.

Use Analytics to Spot What Human Eyes Miss User Behavior Analytics (UBA) and Data Loss Prevention (DLP) tools help surface subtle anomalies—after-hours logins, file transfers, unusual access routes—that are easy to miss otherwise. A Pune-based fintech used behavioral analytics to flag an employee repeatedly sending encrypted files to a personal account. The employee claimed it was for “offsite backup,” but further investigation revealed attempted IP theft. Behavioral AI can flag anomalies across cloud apps, VPNs, endpoints, and collaboration tools. Analysts report time savings of up to 70% during investigations when AI assistants triage alerts and surface contextual patterns.

Treat Culture as a Control Layer Controls fail silently when employees are conditioned to ignore red flags or assume silence is safer. Embedding ethical tone through leadership modeling, anonymous reporting channels, and regular training creates cultural antibodies. In one APAC energy firm, a junior procurement executive flagged a vendor relationship via an anonymous whistle-blower tool, leading to the early unravelling of a collusion ring that had persisted for over a year.

Secure Offboarding as if Breach is Guaranteed Exit events are when many insider incidents peak. Integrating HRIS and IAM systems ensures that resignations or terminations trigger immediate access revocation. Tesla’s 2023 incident, where former employees leaked sensitive data after their departure, is a case in point. A Southeast Asian R&D firm avoided similar fallout by enforcing just-in-time provisioning and de-provisioning protocols linked to HR workflows.

Have an Insider-Specific Response Playbook Most companies have IR plans, but few have tailored playbooks for insider threats, which are often more subtle and reputationally sensitive than external attacks. One U.S. retailer that received a tip-off of employee theft initiated an internal investigation within 48 hours, preserving digital forensics, locking access, and launching containment discreetly. The firm suffered minimal reputational damage, unlike a peer that took weeks to act and landed in the media.

Audit What You Assume Is Working Internal audit/assurance functions should be empowered to do anomaly-led investigations, e.g., looking for outlier spend patterns, non-business hour approvals, or repeated manual journal entries just before quarter close. Even one such “audit sprint” per quarter can raise deterrence significantly and align IA more closely with forensic objectives.

Run Integrity Checks on Third Parties and Employees Collusion risk is highest in procurement, sales, and distribution. Instituting continuous third-party screening, conflict-of-interest disclosures, and employee lifestyle audits (especially in high-risk roles) helps detect early signs. One Indian mid-cap FMCG firm used a third-party integrity check and found that a key distributor was also a silent partner in a logistics vendor, triggering reallocation of contracts.

Conclusion: Don’t Underestimate the Enemy Within

Insider risk is often under-discussed in boardrooms, overshadowed by flashier external threats. Recent cases from banks in India to factories in America demonstrate that misuse of trust and collusion are alive and well in 2024-25, costing businesses dearly. As companies push for growth, they must ensure not to fall into the trap of assuming “it can’t happen here.”

The truth is that as organizations grow, so do the opportunities for insiders to exploit gaps, especially if controls and culture don’t keep up.

The encouraging news is that many insider risks are manageable with foresight and vigilance. By learning from studies like the ACFE’s annual report and industry surveys, companies can understand where they are most exposed. For example, knowing that operations, accounting, and sales departments account for a large portion of internal fraud cases can prompt targeted control improvements in those areas.

Recognizing that collusion multiplies damage fourfold should spur better cross-checks and rotation in high-risk functions. And remembering that employees are often the heroes in detecting fraud emphasizes the value of a speak-up culture and employee training.

Ultimately, effective insider risk management is a balancing act: trust but verify. Companies should cultivate a high-trust workplace but verify that trust through robust controls and oversight. External defenses and cybersecurity matter, but they are not sufficient on their own. Internal vigilance is equally crucial.

In an era of advanced analytics and AI, businesses have powerful tools to monitor for anomalies; combined with human ethics and sound governance, these tools can tip the balance in favor of the honest majority. Mid-sized firms that embrace these principles will not only protect themselves from insider threats but also create a more transparent, accountable environment that investors, regulators, and employees themselves can have confidence in.

In the journey of growth, keeping an eye on the “enemy within” is now an essential part of sustaining success.

As mid-sized listed companies scale, their risk landscape grows more complex. Many still operate with fragmented data systems and ad hoc reporting frameworks. Unlike large enterprises with mature infrastructures, or smaller firms with manageable oversight, mid-sized companies often fall into a blind spot: “too complex to run manually, too constrained to modernize decisively.”

The result? Data exists but is scattered across systems, spreadsheets, and silos. Unstructured, unsurfaced, or untrusted. Risk visibility becomes partial, reporting cycles are reactive, and decision-making is shaped more by instinct than insight.

In this article, we unpack the top root causes behind this challenge. We also outline five strategic remediation moves; practical, scalable steps that mid-sized firms can take to build integrated, resilient, and insight-driven risk data ecosystems.

Because today, risk management is a data problem and solving it is a competitive advantage.

Top Root Causes of Underdeveloped Data & Reporting Frameworks

1 – Absence of a Strategic Data Governance Framework

Most under-developed data environments can be traced to the absence of a robust data governance strategy. Data governance encompasses the policies, standards, and processes that ensure data is accurate, secure, and available. In many mid-sized companies, it is either ad hoc or entirely missing. There’s no centralized framework assigning ownership or standardizing how data must be managed.

How it manifests: Different business units define and handle data independently. For instance, a single counterparty (customer/vendor/partner) may have multiple IDs across systems, distorting their true profile. These inconsistencies stem from the lack of enterprise-wide data definitions, taxonomies, and data catalogs.

Why it persists: Instituting data governance is challenging. It requires cross-functional coordination and often a cultural shift. Mid-sized firms may not necessarily have dedicated a Chief Data Officer or equivalent, leaving IT teams to enforce standards without executive clout. Moreover, some firms perceive governance as bureaucracy that slows down operations. If leadership is unconvinced, they won’t allocate time to build a governance committee or policies.

Impact on risk management: Without strong governance frameworks, companies struggle to aggregate and report risk data effectively leading to poor risk assessments and decision-making. A mid-tier bank without clear data ownership might find that its finance and risk departments use different definitions of “exposure,” resulting in conflicting risk reports. In manufacturing, lack of governance might mean safety incidents or quality defects aren’t logged uniformly, obscuring critical risk trends.

2 – Siloed Systems and Fragmented Data

Mid-sized companies often grow through business silos, each department or subsidiary implementing its own framework, models and structure to suit their maturity curve. The result is fragmented data architecture: customer data in one platform, sales in another, risk metrics in a spreadsheet, and so on, with poor integration between them.

How it manifests: Data silos hinder enterprise-wide visibility.

Attempts to create a “single source of truth” fail if systems don’t talk to each other. A bank’s lending unit and treasury unit might use separate reporting tools, making it laborious to compile an integrated risk report. Or consider a manufacturer where procurement and production each maintain separate inventory records. Without integration, the company cannot accurately assess supply chain exposures or working capital at a consolidated level.

Why it persists: Ironically, despite years of trying to build interfaces, the problem has in some cases worsened – over 40% of companies report that the number of data silos has actually increased, while only ~10% have improved company-wide information access.

Teams might resist sharing data (protecting their turf), and technically it can be challenging (or expensive) to connect legacy systems lacking modern APIs.

Impact on risk management: Data silos are kryptonite for risk oversight. If risk data is scattered, it’s difficult to get a holistic view of the organization’s risk profile. Correlations between risks may go unnoticed as seen in some recent bank failures. In summary, fragmentation undermines any robust risk management framework by preventing timely, accurate data consolidation.

3 – Legacy IT Systems and Technical Debt

The burden of legacy technology, outdated core systems or homegrown solutions that have been patched over time is nothing short of an industry norm. Legacy systems are often inflexible, incompatible with modern data tools, and prone to failure, collectively contributing to underdeveloped reporting frameworks.

How it manifests: A bank might still rely on a decades-old core banking system that wasn’t designed for today’s data demands, requiring batch processes to produce reports (meaning no real-time insight). A manufacturing company could be running an old version of an ERP that lacks modern analytics modules, forcing employees to export data into spreadsheets for analysis.

The prevalence of legacy tech is notable. Nearly 96% of IT professionals in one 2023 survey said they stillneed legacy applications in their environment, and only 4% reported not using any legacy applications.

Why it persists: Replacing core systems is often viewed as risky, expensive, and disruptive. The classic “if it isn’t broken, don’t fix it” mentality.

Technical debt (the cumulative cost of quick-fix IT decisions) accumulates because the company opts for short-term patches over long-term rebuilds.

Impact on risk management: Outdated technology directly impacts risk monitoring and reporting. Legacy systems may not capture the level of data granularity needed for advanced risk analysis (for example, a legacy manufacturing system might not log each production anomaly needed to predict equipment failure risk). They often lack audit trails or modern security, elevating operational and cyber risks.

4 – Cultural Resistance to Change and Data Sharing

Organizational culture plays a pivotal role in the success of data initiatives. Long-standing habits and attitudes create resistance to adopting new data practices or sharing information freely.

How it manifests: Front-line managers may cling to their known and used ‘excel spreadsheets’ and gut-feel decision making, viewing new data systems with suspicion. In many ways, new data systems also expose known but unaddressed failures to the limelight.

Some departments also treat data as a power source to hoard. For instance, the sales team might be reluctant to input detailed client data into a central CRM if they’ve historically managed relationships personally. The XPLM industry survey highlights that two-thirds of respondents said their corporate culture actually favors the emergence of data silos, and 71% admitted that departments “do not want to share their knowledge” across the organization.

This culture can doom data projects; employees might refuse to adopt a new reporting tool, or deliberately bypass official processes (keeping shadow records) because they don’t trust or understand them.

Why it persists: Cultural change is one of the hardest challenges in any organization. Mid-sized companies often have veterans and legacy practices deeply ingrained – “this is how we’ve always done it” can be a mantra. If leadership isn’t actively driving a data-centric culture, middle management is unlikely to enforce it.

Additionally, without adequate training or clear communication of benefits, staff may genuinely fear that new data systems could make their roles redundant or expose their mistakes, thus resisting involvement. There’s also the issue of incentives: if performance metrics don’t reward data sharing or accuracy (and instead only reward short-term results), employees have little motivation to change their behavior.

Impact on risk management: Cultural resistance can sabotage even well-intentioned risk data initiatives. If, say, the risk team implements a new enterprise risk management (ERM) system but business units don’t feed it with timely data, the system becomes an empty shell. An unsupportive culture can nullify the best tools and keep the organization in a reactive stance, where data is seen as a threat or burden rather than a shared asset for informed risk-taking.

5 – Increasing Regulatory and Reporting Complexity

The external environment is raising the bar on data and reporting, and many companies are finding their frameworks lagging behind these evolving requirements. Whether it’s financial regulations, data privacy laws, or sustainability reporting standards, the complexity and volume of reporting expectations have grown exponentially – and mid-sized firms are struggling to keep up.

How it manifests: A regional bank might face new stress-testing data requirements from regulators that its current risk systems cannot support, resulting in frantic efforts to pull the right data. Manufacturing companies now encounter detailed ESG expectations, for instance, European mid-sized listed firms will soon need to comply with the EU’s Corporate Sustainability Reporting Directive (CSRD), tracking metrics from carbon emissions to supply chain due diligence. Many are unprepared.

Why it persists: Unlike large corporations, mid-sized companies typically do not have big compliance departments or the latest Reg-Tech tools. They may be caught off guard by new regulations or find them disproportionately burdensome.

Impact on risk management: Compliance risk becomes a top concern. But beyond compliance, the spirit of these regulations (be it transparency in risk or sustainability) is to drive better decision-making. If a mid-sized firm is only doing the minimum, it likely isn’t leveraging the data to actually improve risk management.

6 – Talent and Skills Gap in Data Analytics

Even with the right tools, organizations need skilled people to build and maintain robust data frameworks. Mid-sized companies often face a talent crunch in this area. They may lack experienced data architects, analysts, or risk data specialists on staff.

How it manifests: The IT team might be small and generalized, without a dedicated data engineer or data scientist. Mid-sized firms often cannot offer the same compensation or career trajectory as large tech firms or banks, leading to a smaller talent pool.

Why it persists: The demand for data and analytics talent has exploded in recent years (with the rise of AI, big data, etc.), and supply has not kept up. Mid-sized companies often have to “grow” their own talent internally, which takes time. Hiring experienced professionals is competitive and costly. Additionally, some mid-tier companies are located outside major tech hubs, making recruitment harder. There’s also the issue of retention.

Impact on risk management: A skills gap can severely hamper risk oversight. Insufficient talent leads to heavy reliance on a few key individuals or external vendors; this concentration is a risk in itself. If those individuals leave or contracts lapse, the organization’s data capability could collapse. Risk professionals in such settings often find themselves doubling as data cleaners and report builders, diverting them from higher-value risk analysis.

5 Strategic Remediation Moves for Mid-Sized Organizations

Mid-sized companies can turn these challenges into opportunities by proactively strengthening their data and reporting frameworks. Below are five strategic remediation moves spanning technology, governance, and people to help resolve or mitigate the above root causes. These strategies are interrelated and can be pursued in parallel:

1 – Establish a Robust Data Governance Framework with Executive Ownership

Firms should formalize a data governance program that defines clear roles, responsibilities, and policies for data management. This also means appointing accountable data owners/stewards in each domain. To succeed, governance cannot be an IT-only initiative.

It needs top-down endorsement and enforcement. Leadership should treat data as a strategic asset, regularly reviewing data governance progress just as they would financial results.

The key is also continuous improvement: governance isn’t a one-time project but an ongoing program that adapts as the company grows and regulations change.

2 – Invest in Modern, Scalable Data Architecture and Tools

A strategic upgrade of technology can pay huge dividends. Mid-sized organizations should evaluate and invest in scalable data infrastructure that could involve moving to cloud-based platforms, implementing a unified data warehouse or lake, and deploying business intelligence (BI) and reporting tools that automate data aggregation and visualization.

Modern cloud solutions are increasingly accessible to mid-market companies (often offered in modular, pay-as-you-go models), lowering the barrier to entry. Key considerations would be toprioritize integration-friendly solutions and adopt tools that reduce manual work, such as ETL for moving and reconciling data

3 – Strengthen Data Talent and Literacy Across the Organization

People are the linchpin of any data strategy. Companies should invest in their human capital by both acquiring and developing data skills. If hiring full-time is difficult, engaging external consultants or service providers on a project basis can jump-start initiatives while transferring knowledge to internal staff.

On the development front, companies should launch data literacy programs so that employees at all levels become more comfortable with data and analytics tools.

A focus on talent and literacy sends a message that data isn’t just the IT team’s job, it’s everyone’s responsibility.

4 – Foster a Data-Driven Culture with Strong Change Management and Incentives

Leaders should consistently communicate the importance of data in achieving the company’s goals, and celebrate data-based decision making.

Some firms establish cross-functional teams or “communities of practice” around data, which break down silos by design. It can also help to start with small wins. Pilot the new framework in one department, refine it, and then expand, so people see proven benefits.

A data-driven culture also means employees become more likely to report issues or anomalies when they occur, rather than hiding them, because they know management wants to hear the data even if it’s bad news.

In essence, technology and processes might provide the tools, but culture is the soil in which a data-driven enterprise either withers or thrives.

5 – Align Data Initiatives with Risk Management and Compliance Objectives

Lastly, mid-sized organizations should explicitly try and link their data framework improvements to their broader risk management and compliance goals. In practice, this means using risk-based criteria to drive data projects: focus on the data that matter most for the company’s risk profile and regulatory requirements.

Some mid-sized firms establish a Risk and Data Steering Committee that meets regularly to ensure data initiatives are evaluated in terms of risk reduction and compliance impact. Additionally, keep an eye on upcoming regulations and proactively build capability to meet

Ultimately this alignment creates a virtuous cycle: good data feeds into good risk management, which identifies areas for improvement, which in turn drives further data enhancements. By making risk management a key outcome of data strategy, companies ensure their data framework upgrades truly fortify the organization’s resilience and not just its operational efficiency.

Conclusion

Transitioning to a mature data and reporting framework is undoubtedly a journey, not an overnight fix. However, by understanding the root causes behind their current shortcomings, organizations can target their efforts more effectively.

The challenges outlined often interact, but the good news is that the remediation moves are mutually reinforcing as well. With committed leadership, smart investments in technology, empowered people, and a culture that values information, companies can evolve their data practices significantly. The payoff is more than just better reports. It is improved risk foresight, stronger compliance, and enhanced decision-making agility.

Sources:

Basel Committee on Banking Supervision (BCBS 239) progress reports (2023)

BIS reports on supervisory expectations for risk data frameworks

Case studies: Silicon Valley Bank collapse analysis, 2023 U.S. Senate testimony and Fed reviews

Sero Group: Implementing Data Governance for Small and Medium-Sized Businesses

XPLM (2023): Study on Enterprise Data Silos and Cultural Resistance to Data Sharing

Gartner, Forrester, and IDC insights on enterprise data architecture adoption

QBE Global Risk Index (2023): Mid-Market Risk Prioritization and Preparedness Survey

Hyperproof GRC Benchmark (2024): Risk and Compliance Operations in Fragmented Environments

Sage (2023): SME Cloud and Sustainability Technology Trends Report

IDC SMB Tech Pulse (2023–24): Cloud adoption rates and tech spend forecasts for mid-sized firms

McKinsey Digital: The Value of a Scalable Data Architecture for Mid-Sized Enterprises

World Economic Forum: 2023 Global Talent Outlook

Udemy for Business: Skills Gap in Data Literacy 2023 Report

Let us for illustration purposes understand the approximate scale of the compliance requirements for mid-sized enterprises in India.

India’s regulatory ecosystem has tens of thousands of requirements, over 69,000 unique compliance requirements across 1,536 laws by one count. These are not abstract numbers; they translate into a daily grind of filings and checkpoints.

A medium-sized manufacturing company in India, for example, might need to comply with 5,500+ distinct regulations, whereas even a small manufacturing unit must follow around 750 regulations. These include everything from labor law registers and tax returns to factory safety displays and environmental permits.

TeamLease Regtech, a compliance technology firm, estimates that an Indian MSME with just over 150 employees faces 500–900 applicable compliance requirements. It’s no surprise that business owners feel the weight of this “control bloat” in their operating costs.

Although the organizations are free to assess their own risk appetite and calibrate approach to suit a “Risk Based Approach”, in reality, the fear of potential non-compliance leads to excessive compliance burden.

Rising Compliance, Spiraling Costs, Unclear Value

One of the clearest signs of “compliance fatigue” is the growing cost of compliance, relative to its perceived benefit. Compliance budgets have been rising rapidly, often without commensurate clarity on what risks are actually being mitigated or value gained.

Despite massive compliance expenditures in certain industries, breaches and fines continue unabated. For instance, global banks collectively paid billions in penalties in recent years even as their compliance departments grew larger than ever. Regulators have openly noted that they remain unimpressed by the amount of money spent on compliance, what matters are outcomes. If compliance spending doesn’t translate to fewer incidents, its ROI is fundamentally in question.

Across industries, leaders are asking hard questions: “What are we really protecting with all this spending?” It’s often difficult for compliance officers to answer with hard data. Ideally, compliance investments protect the business from fines, fraud, data breaches, safety incidents, reputational damage, etc. But quantifying the absence of a crisis is challenging. Compliance’s success is often that “nothing bad happened,” a counterfactual that’s tricky to monetize.

In fact, most organizations don’t even measure their compliance spending in a holistic way. A 2023 survey by Thomson Reuters found that 45% of firms did not monitor the total cost of compliance across the organization in any form. Without tracking cost, it’s nearly impossible to calculate ROI. It’s not surprising, then, that compliance teams struggle to demonstrate tangible value.

The bottom line: Many organizations feel trapped in a compliance cost spiral; pouring more and more money and effort in, without a clear picture of risk reduction or business value out. Business leaders don’t want to write blank checks for compliance; they want to know their investments are actually protecting the company’s most critical assets and stakeholders.

Audit Overload and Tick-Box Compliance Culture

Why Leaders Are Concerned

When we weigh fragmented initiatives, audit overload, ballooning costs, reactive spending, and staff burnout, it becomes clear why many organizations see a cost-benefit imbalance in their compliance programs.

The benefits (risk reduction, avoidance of fines/incidents, improved reputation), while very real, are often opaque and lagging, whereas the costs are immediate, tangible, and rising. This imbalance is leading some executives and board members to question whether they are getting value for money from compliance.

In blunt terms, if we doubled our compliance spend in the past 5 years, are we twice as safe? Or as one expert framed it: “What is the probability that the usual GRC investments are genuinely protecting the business?”. If that probability is low or unknown, it signals a problem in how the program is structured or measured.

Business leaders don’t want compliance to be a necessary evil; ideally, they want it to protect what truly needs protecting and enable the business to thrive. The challenge ahead is how to rebalance the equation so that the compliance function’s value is as plain as its cost.

Improving ROI Clarity: Strategies for Better Compliance Value

Despite the daunting picture, there are concrete steps organizations can take to rebalance their compliance efforts and improve clarity. Below are several actionable recommendations and strategic shifts that can help transform compliance from a fatigue-inducing cost center into a more efficient, value-driven function:

1 – Adopt a Risk-Based, Strategic Approach:

Rather than treating all compliance activities as equally critical, prioritize resources toward the risks that could most seriously harm your organization. This means clearly answering the question, “What are we really protecting?” Is it customer data? Financial integrity? Safety of employees? Once you identify your crown jewels and top threats, align compliance controls to those areas first.

A risk-based approach also involves defining your risk appetite (what level of risk you’re willing to accept). This helps right-size compliance efforts; in areas of low risk, avoid over-engineering costly controls that don’t add value. By focusing on what truly matters, you can start to quantify benefits (e.g. “we reduced the probability of a major data breach by X% through these controls”) and thus demonstrate ROI in terms of risk reduction.

2 – Consolidate and Streamline Programs:

Break down the silos between various compliance initiatives. Often different teams manage overlapping requirements with separate processes and tools.

Conduct a program audit to identify overlap and inefficiency. You may find, for example, multiple teams separately assessing vendor risk or multiple tools tracking similar control inventories. Consolidating these efforts not only cuts cost but improves consistency.

Consider establishing an integrated GRC (Governance, Risk, Compliance) framework where a single system maps all controls to relevant regulations. This allows one control (say, an access security control) to satisfy multiple requirements at once, reducing duplicate work.

Streamlining should also extend to audits: whenever possible, use a single evidence repository so that one piece of evidence can serve multiple audit objectives, alleviating audit fatigue.

3 – Leverage Technology and Automation:

Invest in modern compliance tools that automate and improve visibility. According to Accenture research, 93% of compliance leaders agree that AI and cloud-based compliance tools can remove human error and automate manual tasks, boosting efficiency.

Some areas to target with technology include: continuous monitoring of controls, workflow tools for policy management and attestation, and data analytics to detect compliance issues early. However, technology is not a silver bullet. It should be implemented alongside process improvements, not just layered on top of bad processes.

4 – Define Metrics and Communicate Value:

To make ROI clear, define key performance indicators (KPIs) for your compliance program that relate to both cost and benefit. It’s notable that nearly half of the firms do not monitor their cost of compliance at all; simply starting to measure it is step one. Next, translate compliance outcomes into the language of business. Even if not perfect, they signal that the compliance function is evaluating its own effectiveness.

5 – Foster a Culture Beyond Box-Ticking:

Cultural change is critical. Tone at the top matters. Leadership should emphasize that compliance is about protecting the company and its stakeholders, not just pleasing regulators.

Make compliance part of performance evaluations for everyone, not as an extra burden but as an expected aspect of good business practice.

When compliance is culturally rooted, people are less likely to see it as an external imposition and more as a shared value.

Engaged employees are the best defense and also the best champions to demonstrate that compliance work has real impact.

6 – Right-Size the Compliance Organization:

Leverage external expertise strategically. For example, use outside counsel or consultants for niche regulations or periodic compliance program reviews, rather than carrying that full expense in-house year-round.

This can provide access to expert knowledge on demand and help answer tricky ROI questions.

At the same time, cross-train team members on different aspects of compliance; a well-rounded team can handle a wider range of issues, improving efficiency.

7 – Align Compliance Objectives with Business Goals:

One way to underscore ROI is to tie compliance initiatives directly to business objectives. For example, if a company’s goal is to expand into European markets, frame the enhancement of your privacy compliance (GDPR, etc.) as an enabler of that expansion (gaining customer trust and avoiding legal roadblocks).

If the business is embracing digital transformation, position your cybersecurity compliance upgrades as protecting that digital innovation (thus avoiding costly setbacks from breaches). By framing it this way, you shift the narrative from “compliance is a cost we must bear” to “compliance is helping us achieve X business outcome securely.”

Consider building “compliance by design” into product development and strategy, ensuring that new initiatives consider regulatory requirements from the start.

8 – Review and Reduce Bureaucracy:

Periodically conduct a “clean-up” exercise. Many compliance programs accumulate layers of checks over time (often as reactions to past problems) and never shed any.

Sometimes, simplifying a control or combining two steps into one can maintain effectiveness and save hundreds of person-hours. Every hour saved is essentially money saved or re-allocated to more meaningful work. This improves the perceived ROI because people see that compliance is mindful of efficiency and not just adding procedures endlessly.

Implementing the above strategies requires effort and commitment, but the pay-off is two-fold: reduced fatigue and higher ROI clarity. Firms that have pursued such improvements report not only cost savings, but a stronger confidence among leadership that compliance investments are worthwhile.

Conclusion

Companies today find themselves juggling a multitude of regulatory demands, from financial controls to data privacy to ESG, with teams that are overloaded and budgets that seem to grow faster than the perceived benefits. The current state in many organizations is fragmented compliance efforts, reactive fire-fighting, and a culture of ticking boxes to get through audits, all contributing to high costs and murky value. Mid-size firms feel this pain acutely as they shoulder enterprise-level rules with far fewer resources.

Yet, it doesn’t have to remain this way. By reimagining compliance through a strategic lens, focusing on risk-based priorities, integrating programs, leveraging technology, and fostering a compliance-positive culture, businesses can turn compliance into a more streamlined, proactive, and yes, valuable part of operations.

In the end, the goal is to establish compliance programs that confidently answer the ROI question. That means being able to articulate, at a high level: Here’s what we’re protecting, here’s what it would cost if we failed, and here’s how our compliance efforts prevent that.

Sources:

Wipro Sustainability Report FY 2023-24 – warning against “compliance fatigue” leading to a checkbox mentality

Mid-sized companies across the globe are grappling with an increasingly complex risk landscape. From cyber threats and supply chain disruptions to regulatory changes and market volatility, operational risks today are more interlinked across business functions than ever before.

Yet, many of these organizations lack a harmonized risk language and accountability, a shared, enterprise-wide way to understand, categorize and monitor risks. Instead, each department often speaks its own dialect of risk, using different taxonomies and sometimes, tools to monitor. The result is that critical issues can go unspoken, miscommunicated across silos, leading to unclear ownership of risks, duplicated compliance efforts, and missed early warning signs of trouble.

What is a “common risk language”?

In simple terms, it’s a standardized vocabulary and classification of risks that everyone in the organization uses. This involves agreeing on a risk taxonomy, risk ratings and terms across all teams. The purpose of a common risk language is to ensure that a finance manager, an IT analyst, and an operations supervisor all mean the same thing when they discuss “high operational risk” or a “compliance issue”. A a common framework enables people with diverse backgrounds to communicate effectively about risk and identify issues more quickly.

According to one benchmarking survey, teams managing risk in silos reported spending nearly 38% of their time on administrative tasks (assembling reports, updating spreadsheets) and the vast majority said at least one-third of their effort went to repetitive manual work. These inefficiencies directly translate to higher compliance costs and lost productivity.

One common symptom is unclear risk ownership. For example, consider a mid-sized manufacturing firm. The operations team tracks safety incidents and supply disruptions, the IT team handles cybersecurity threats, and CISO monitors regulatory issues. When a critical supplier suffered a cyber breach, operations labeled it a supply chain issue, IT labeled it a vendor cyber risk, and CISO saw a third-party data privacy concern.

Another example ailing many financial institutions pertains to preventing, detecting Money Mules (Money mule risk refers to the threat posed to a financial institution when its accounts, systems, or services are exploited knowingly or unknowingly by individuals, to move illicit funds, thereby exposing the institution to fraud losses, regulatory breaches, and reputational damage.)

Who truly owns this risk? Is the fraud risk team or the AML Compliance team or the cyber team or the first line of defense? Money mules are a classic case of an interconnected risk without a common language. Multiple functions in the same organization perceive the risk differently and hence, are never able to solve the root cause issues are a singular unified view. Without a unified view, early indicators that might have been obvious in say, a consolidated dashboard, remain scattered.

Since there are no common taxonomies linking these perspectives, no single owner is alerted to the full picture. This overlap and ambiguity mean everyone assumes someone else is mitigating the problem. The early warnings are hence, often missed amidst the fragmented reports.

The problems exacerbate in case of un-regulated sectors.

Why a Common Risk Language Matters:

Aligned Risk Appetite and Decision Making: A common risk language helps align the organization’s risk appetite with operational decisions. Risk appetite, the level and type of risk a company is willing to accept in pursuit of its objectives, is typically set at the top. With a unified taxonomy, management can define risk appetite in concrete terms for each risk category, and everyone from the board to the business units understands it the same way. This means decisions on the ground are made with a clear understanding of how they fit the company’s risk tolerance.

Clear Ownership and Accountability: With the unification, every major risk category has an owner and stakeholders who all understand what falls under that risk. There’s less chance of “grey area” risks being unowned. Responsibilities can be assigned without ambiguity ensuring someone is watching each risk and accountable for responding.

Enterprise-Wide Visibility: Using one risk language allows aggregation of risk data across the whole company. Executives can see the full risk profile without blind spots. Early warning indicators become more apparent when all inputs feed into one picture. Patterns (like similar issues cropping up in different regions or departments) can be detected via the common categories. This holistic view is essential for spotting systemic risks that individual silos might overlook.

Efficiency and Reduced Duplication: Standardizing risk categories and reporting streamlines processes. The same risk does not need to be assessed in triplicate by different teams; one assessment can serve multiple purposes. Controls and mitigations can be designed to address multiple related risks at once. This cuts down the repetitive administrative burden. In mid-sized firms where resources are limited, this efficiency can be a game-changer, freeing staff to focus on high-value risk mitigation.

Improved Communication and Collaboration: A shared vocabulary breaks down communication barriers between functions. In day-to-day operations, this means cross-functional teams can come together quickly around emerging issues, because they have a common reference point. Stakeholders from different domains can contribute insights without talking past each other, leading to more robust risk assessments.

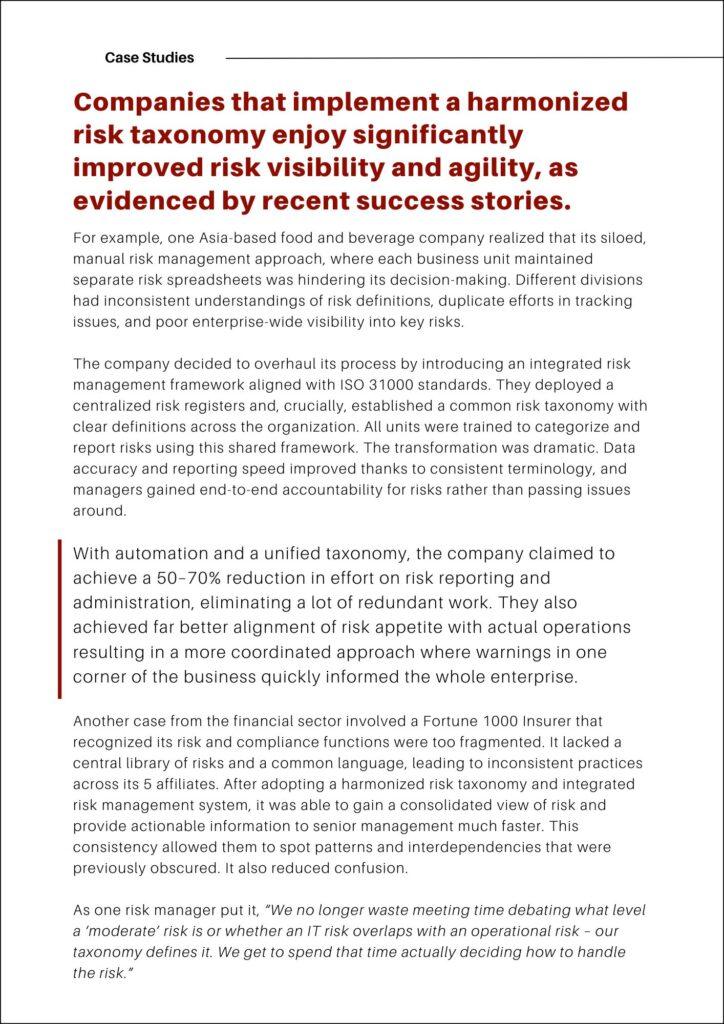

A Contrast: Harmonized Taxonomy in Action

Building a Common Risk Language: Practical Steps for Mid-Sized Companies

Implementing a harmonized taxonomy may sound daunting, but it can be achieved with a series of practical, staged steps. Mid-sized corporates, in particular, should tailor these steps to their scale and culture, focusing on enabling cross-functional collaboration without excessive bureaucracy.

Below is a roadmap to strengthen enterprise-wide risk insight and decision-making through a common language.

1 – Inventory and Reconcile Existing Risk Terminologies:

Identify overlaps and gaps – Gather the risk lists and terminologies currently in use across departments (e.g. finance risk register, IT risk log, HR compliance checklist, etc.). It’s common to find different names for essentially the same risk. For instance, “data leak” in IT, “confidentiality breach” in legal, and “privacy compliance failure” in compliance might actually refer to overlapping risk events.

Draft an initial unified risk taxonomy – Form a small working group with representatives from key functions to review and start mapping equivalences. Leverage industry frameworks as a starting point, for example, ISO 31000 or COSO ERM categories but customize them to fit the company’s context. This collaborative approach brings deep expertise from each area and ensures the taxonomy isn’t imposed top-down but rather agreed upon.

Develop a Common Risk Glossary and Definitions – For each risk category and sub-category in the taxonomy, write down a clear definition and examples. This becomes the glossary of the common risk language and a common rating criterion.

2 – Assign Clear Risk Ownership and Governance

Assign Risk Owners – With the taxonomy in place, assign risk owners for each major category or for specific key risks. In a mid-sized company, a single executive or senior manager might own multiple related risks (for instance, the Head of Operations might own Supply Chain and Safety risks, the CFO might own Financial and Compliance risks, etc.). The important part is that it’s documented and communicated.

Establish a cross-functional working groups – Set up risk workking group that meets regularly to discuss risks enabled through the common language. Having this governance structure formalizes the common language, it’s where everyone “speaks risk” together. It helps break the historical silo mindset and replace it with a culture of information-sharing.

3 – Implement Enabling Tools and Central Risk Register

Establish a single source of truth – This could be as simple as a shared spreadsheet or database in smaller companies, or a module in GRC (Governance, Risk & Compliance) software for those who have it. The key is that all departments log their identified risks, incidents, and mitigation plans in this central repository using the agreed taxonomy and ratings.

Provide visibility to the central source of truth – This central risk register gives everyone visibility into risks across the enterprise. It also simplifies reporting; one can generate an enterprise risk dashboard from it for management or board reporting, instead of manually compiling data.

4 – Integrate Risk Discussions into Operational Processes:

Having a common language and tool is half the battle; the other half is making sure it’s used in decision-making. Mid-sized firms should embed the common risk language into their routines. For example:

Department heads can be required to include an update on key risks (using the common categories) in their monthly reports.

Project proposals can have a section assessing risks in common language terms.

Incident post-mortems should map causes and follow-up actions to the taxonomy categories.

Gamify or use simple checklists to guide staff on identifying and reporting risks consistently.

The goal is to avoid situations where only risk managers talk about risk. Instead, every team uses the common language in their context.

5 – Link the Common Language to Risk Appetite and Strategy:

Articulate risk appetite – Ensure that the company’s risk appetite is articulated in the same terms as the risk taxonomy. This practice directly ties operational risk oversight to strategic goals and thresholds. It also helps in aligning mitigation efforts with what the company cares about most.

Periodically review enterprise risk profile – Companies should review these appetite statements periodically in their risk committee and adjust as necessary (for instance, if entering a new market or launching a new product, adjust appetite and categories accordingly).

6 – Continuous Education and Refinement:

Implement Ongoing Training – Conduct periodic workshops or scenario drills where cross-functional teams practice responding to a hypothetical risk event using the shared framework. The risk landscape also changes so the common language must evolve too.

By following these steps, mid-sized enterprises can gradually build a common risk language that permeates the organization. This is as much a cultural initiative as a technical one. Leadership should articulate the “why”; explain to all staff that the company is establishing a common risk language so that everyone can work together to safeguard the business. Teams start to see how their concerns connect with others’.

Mid-sized companies may not have the massive risk departments of large corporations, but they can absolutely achieve world-class risk oversight through this exercise. When risks stop being described in incompatible ways and instead are discussed on a shared platform, previously “unspoken” priorities become clear. Early warning signals emerge from noise. Compliance efforts become more about insight than paperwork.

In an environment of ever-interconnected risks, establishing this shared understanding is fast becoming not just a best practice, but a necessary priority for sustainable growth.

As the old proverb goes, “if you want to go fast, go alone; if you want to go far, go together”. A common risk language ensures that a company’s departments go together, equipped with unified insight, as they navigate the risks on the road ahead.

Sources:

Boultwood, B. How to Develop an Enterprise Risk Taxonomy. GARP (2021) – Importance of a hierarchical common risk language for ERMgarp.orggarp.org.

LogicGate Risk Cloud. The Language of Risk (2021) – Benefits of a shared risk vocabulary; 50% of companies lack consistent risk data/languagelogicgate.comlogicgate.com.

Chambers, R. Break Down Silos for Visibility Into Enterprise Risk. MIT Sloan Management Review (Feb 2025) – 86% of risk professionals say silos hinder risk management; need for holistic approachsloanreview.mit.edu.

OneTrust Blog. Who Owns Third-Party Risk: Breaking Down Silos (Mar 2022) – Risk silos create duplication of efforts, analysis gaps, lack of knowledge sharingonetrust.com.

Hyperproof. 2025 IT Risk & Compliance Benchmark Report (Oct 2024) – Data silos link to higher breach frequency; 46% of siloed-risk firms had breaches vs 30% with integrated approachhyperproof.io. Also, siloed teams spend ~38% time on admin taskshyperproof.io.

MetricStream Case Study. Almarai – Enterprise Risk and BCM (2020) – Fragmented approach led to inconsistent risk understanding, limited visibility, duplicate workmetricstream.commetricstream.com; introducing common risk taxonomy improved data accuracy, visibility and cut effort by 50–70%metricstream.commetricstream.com.

MetricStream Case Study. Fortune 1000 Insurance Co. GRC Journey (2021) – Lack of common risk language caused inefficiencies, solved by centralized taxonomy and platformmetricstream.com.

Chakraborti, A. Challenges of ERM Implementation in India (Jan 2024) – Mid-sized enterprises struggle with resource constraints for risk managementlinkedin.com.

DeLoach, J. Using a Risk Model as a Common Language. Corporate Compliance Insights (2014) – Purpose of a common risk language is to ensure completeness in risk identification and effective communicationcorporatecomplianceinsights.com.

Risk management failures in mid-sized and emerging companies have made headlines from Silicon Valley to Mumbai, often tracing back to a troubling disconnect between boardroom understanding and on-the-ground realities. This “board-versus-operational reality” gap in risk oversight has tangible consequences; from financial losses and regulatory penalties to reputational damage. A recent consulting survey indicated nearly 55% of board members say their company’s risk management struggles to keep pace with business strategy changes.

In an era of rising uncertainties, board members and independent directors are expected to serve as crucial sentinels, yet their effectiveness is often hampered by cultural and informational barriers. As a part of this series, we explore in this article as to why mid-sized enterprises are prone to governance gap, the real-world fallout when it goes unaddressed, and how boards can close the chasm between the view from the boardroom and the operational reality on the ground.

Understanding the Oversight Gap

Every corporate board has a fiduciary duty to oversee risk, but there’s often a disconnect between what boards believe about risk management and what’s actually happening within the organization. In many mid-sized firms, boards receive periodic risk reports and updates that paint a reassuring picture. Risks identified, controls implemented, compliance boxes checked. Yet the day-to-day reality in business units or project teams can be very different. Metrics and reports presented to the board may be incomplete or overly optimistic, leading to a false sense of security at the governance level.

Boards often overestimate risk management effectiveness due to incomplete information and structural weaknesses, leaving mid-sized firms vulnerable to crises. This gap is not due to negligence or indifference from boards, but rather structural and cultural challenges.

Root Causes of the Gap

Information Asymmetry: Senior executives may filter what they escalate to the board, and mid-level managers might downplay or fail to report issues upward, especially in a culture that ‘shoots the messenger’.

Limited Risk Expertise: Limited expertise in specific risk areas often exacerbates the problem. If directors aren’t well-versed in emerging risks (be it cybersecurity, regulatory compliance, or operational safety), they may not know the right questions to ask or may accept vague assurances. In fact, one analysis observed that a lack of operational risk expertise can make board members reluctant to stray from their domain.

Siloed Reporting: Operational risks are often tracked inconsistently, failing to reach the board in a meaningful way. Without the right data and Key Performance Indicators (KPIs), they might not realize the true magnitude of certain risks.

Differing Perspectives & Priorities: It helps to recognize that boards and operational teams often view risk through different lenses requiring better communication to align high-level oversight with ground-level realities.

Why Mid-Sized Companies Are Especially Vulnerable

Weak Risk Framework: Large multinational corporations often have extensive risk management frameworks, dedicated risk officers, and layers of oversight. In contrast, small and mid-sized enterprises (SMEs) frequently operate with leaner structures which can widen the board-operational gap. Research shows that many mid-sized companies do not have fully defined Enterprise Risk Management (ERM) programs due to cost constraints, limited resources, and fewer dedicated risk professionals.

Lean Structures: Often, employees wear multiple hats; for example, the finance head might also oversee compliance, or operations managers double as safety officers. This can lead to gaps in expertise and bandwidth when it comes to systematically identifying and mitigating risks. The board might assume that “someone in management” is handling risk, but in reality, risk responsibilities can fall through the cracks in a mid-size organization’s structure.

Rapid Growth: Mid-sized firms are frequently in high-growth mode. They are expanding into new markets, launching products, or undergoing digital transformation, all of which introduce new risks. However, governance processes in these companies often lag behind their growth. A post-mortem by regulators on Silicon Valley bank observed that the bank’s growth far outpaced the abilities of its board and management to install a suitable risk control infrastructure.

Cultural Pressures: A ‘Business Today’ magazine analysis of recent startup scandals noted a “convenient lack of oversight from boards, as start-ups get caught up in the rat race of growth over profits”. Mid-sized enterprises, especially those led by founders or family owners, can have tight-knit cultures with strong top-down influence. If the leadership’s emphasis is on aggressive growth or hitting targets “at all costs,” employees may feel pressure to prioritize results over risk compliance.

Weak Internal Controls: Mid-sized firms often lack the robust internal controls and audit functions that larger firms use to catch issues early. Risk assurance processes in a smaller company might be outsourced or minimal, and risk reporting may not be integrated company-wide. This means the board’s usual safety net, internal audit and compliance reports, may not be effective.

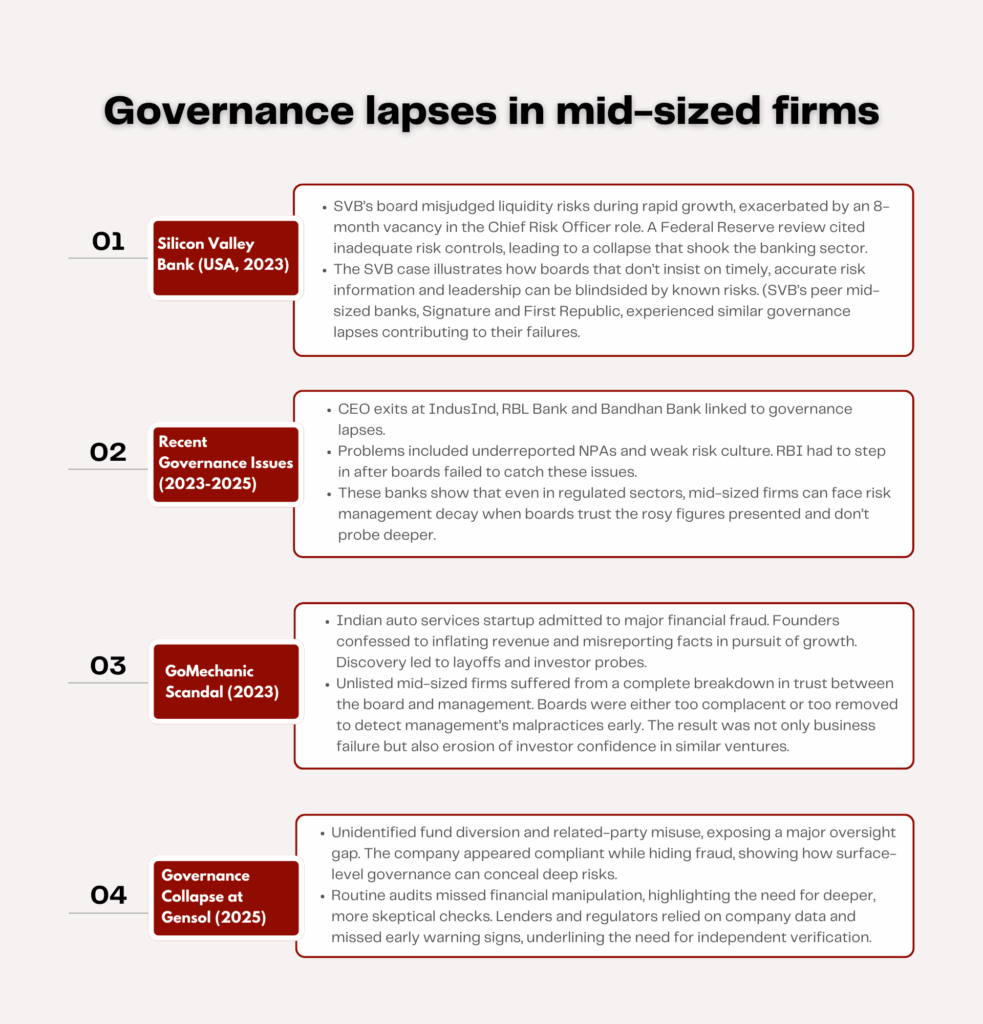

Governance lapses in mid-sized firms lead to serious failures, underscoring the need for boards to bridge the oversight gap. Recent cases illustrate how the board-operational disconnect fuels crises:

These examples across different sectors highlight the critical gap between boards oversight and operational realities, where incomplete knowledge of day-to-day operations led to risk management failures. Despite having boards and risk policies on paper, governance breakdowns allowed small issues to escalate into major crises. For mid-sized and emerging companies, closing the board-operations gap in risk oversight is not just a best practice but a strategic necessity for survival and success.

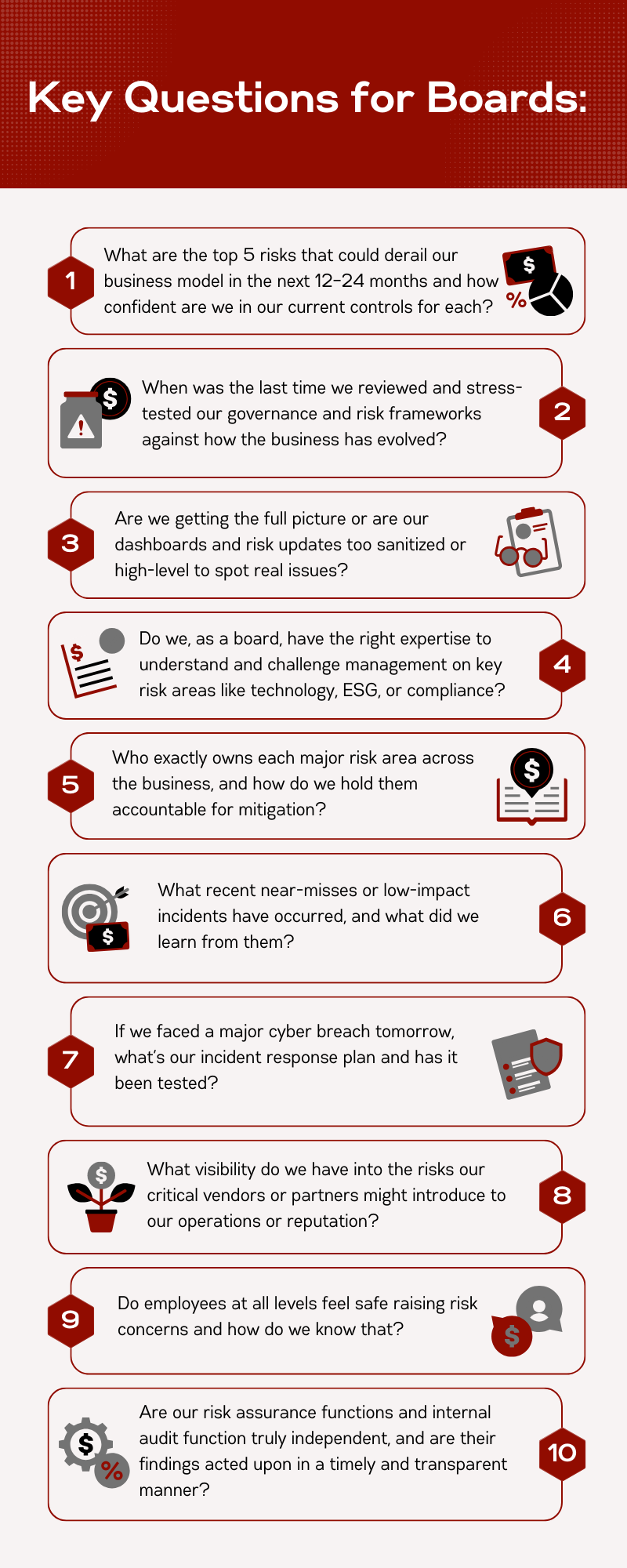

Closing the Gap: Practical Steps for Boards to Enhance Risk Oversight

Bridging the divide between boardroom perception and operational reality in risk management requires concerted action. Boards of mid-sized and emerging companies can take practical, actionable steps to enhance the sanctity of their risk oversight role. These steps span tools and technology, structural and process improvements, and cultural shifts. Below are key recommendations for boards and their companies:

Unfiltered Communication: Boards must insist on clear and candid risk reporting. Boards should demand that risk reports be forward-looking, impact-focused, and unfiltered. Instead of high-level summaries that gloss over issues, reports should explicitly connect risks to business outcomes. This can be done through reviewing “risk dashboards” that include key risk indicators, incident logs, and mitigation status updates for major / emerging risks.

Strengthen risk governance structure: Many mid-sized companies suffer because no single leader is accountable for enterprise-wide risk – plugging this gap is vital. Establish regular sessions where the risk officer and internal audit head can speak to directors without senior management in the room, fostering open communication.

Translate Technical Risks & Elevate risk discussions: Operational details (e.g., “unpatched firewalls”) should be framed in business terms (e.g., “potential $2M loss from a breach”).

Make risk a standing priority at every board meeting. Just as financial performance and strategy are regularly discussed, insist that significant operational and strategic risks get airtime in proportion to their importance. Boards could also consider scenario planning and deep-dives: pick a few “what if” scenarios.

Leverage Technology and Data for Risk Monitoring: In today’s digital age, even mid-sized companies can afford tools to enhance risk oversight. Boards should encourage management to utilize risk management software, dashboards, and data analytics to gain real-time visibility into risks. According to a 2025 survey, 76% of mid-market businesses already use technology in some aspect of risk management, but only 11% have fully integrated. There is immense room to grow here.

Fostering risk aware culture through appropriate tone at the top: Perhaps the most critical yet intangible fix is cultural. The board and executive leadership must set the tone that risk management is everyone’s responsibility and is valued. Leadership should visibly recognize and reward teams that identify and manage risks well, turning risk management successes into learning moments company-wide. Conversely, there should be accountability when risk processes are ignored or warnings silenced. The board could ask for a “Risk Culture” assessment. If results show problems say, the board must push management to address this through appropriate training.

As experts advise, boards should exercise an “inquisitive mindset; digging deeper, challenging assumptions, and encouraging open communication. All before adverse events materialize.”

In essence, bridging the gap requires aligning these perspectives. When governance and implementation are in sync, Boards can anticipate issues and support management in addressing them proactively, rather than cleaning up surprises after the fact.

The Strategic Role of Independent Directors in Risk Oversight

Independent directors are critical for objective oversight, challenging assumptions and fostering a risk-aware culture. Independent directors bridge the gap by:

Asking Tough Questions: Free from management ties, they probe operational realities (e.g., “Are cybersecurity resources adequate?”).

Bringing Expertise: Directors with cyber or compliance backgrounds enhance oversight, reducing financial irregularities (per governance surveys).