Introduction

When it comes to risk management, mid-sized listed companies often focus on external threats—cyberattacks, market volatility, regulatory changes. Yet, one of the most damaging risks can come from within: insider risk, where employees or trusted parties collude to commit fraud.

Insiders are behind a significant share of corporate fraud and data breaches, costing businesses millions. A recent global study by the Association of Certified Fraud Examiners (ACFE) found that organizations typically lose 5% of their annual revenue to occupational fraud (which by definition involves insiders), with total losses exceeding$3 billion in the cases studied. The median loss per internal fraud case was$145,000—a hefty hit for a mid-sized firm. Losses as a percentage of revenue tend to be higher in smaller organizations than in large enterprises.

In short, the threat from within can be as damaging as any external attack, yet it doesn’t always get the attention it deserves.

Defining the Insider Threat Spectrum

Insider threats span a spectrum of behaviors—malicious, conflicted, fraudulent, or negligent—each with distinct triggers and impacts. Understanding these typologies is essential for proactive risk management.

Malicious Insiders

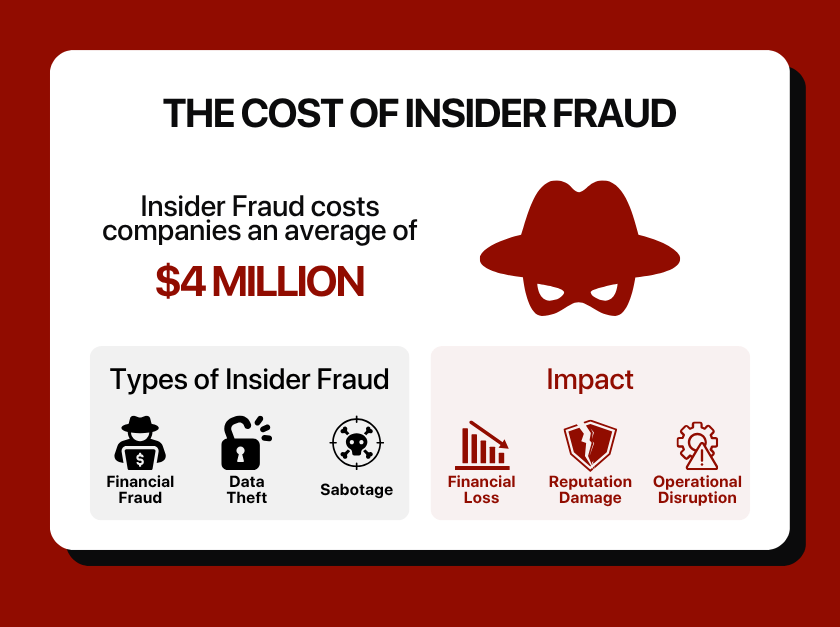

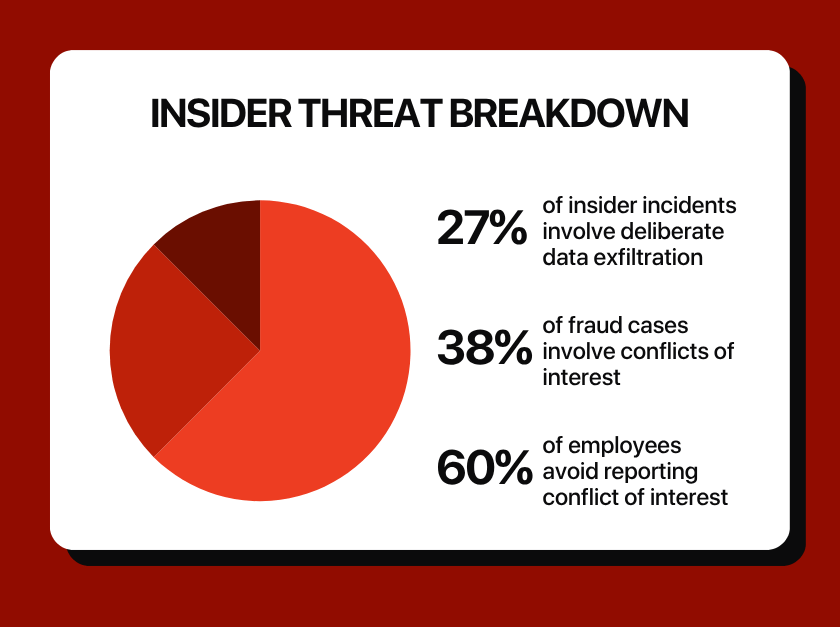

Malicious insiders intentionally harm the organization through actions like data theft or sabotage. Triggers include financial distress, disgruntlement, or external coercion. For example, an IT administrator at a mid-cap tech firm might leak customer data to a competitor for financial gain, exploiting elevated access privileges. The 2025 Ponemon Institute report noted that 27% of insider incidents involve deliberate data exfiltration, costing$15.3 million on average.

Conflicted Insiders

Conflicted insiders prioritize personal gain through undisclosed vendor ties or related-party deals. Triggers include personal relationships or financial incentives. A 2023 EY Fraud Survey found 38% of fraud cases in mid-caps involve conflicts of interest, such as a procurement officer awarding contracts to a relative’s firm without disclosure. Weak oversight exacerbates these risks, as mid-caps often lack automated vendor screening.

Silent Fraud

Silent fraud involves subtle misconduct, such as skimming, expense misreporting, or privilege abuse, often enabled by weak controls. For instance, an employee inflating expense reports might go undetected without automated reconciliation, draining resources over time.

Negligent Insiders

Negligent insiders cause harm through human error or poor control hygiene, such as clicking phishing links or mishandling sensitive data. For example, an employee downloading malware via an unverified link could expose customer data, leading to costly breaches.

Third-Party Threats

Contractors or vendors who have inside access can compromise security, either intentionally or via lax practices.

Why Growing Companies Are Especially Vulnerable

Growing companies are often large enough to present ample opportunities for internal fraud, but they may not yet have the robust controls and corporate governance that mature enterprises deploy. Rapid growth can strain internal processes. New departments, higher transaction volumes, and more employees may outpace the development of a strong control environment.

Informal Trust Culture

Tight-knit teams often prioritize harmony over scrutiny. Employees hesitate to report colleagues, fearing conflict or disruption. Without formal escalation channels, early red flags go unnoticed. A study found 60% of employees avoid reporting conflicts of interest to preserve team dynamics, underscoring how silence becomes the norm in trust-heavy environments.

Limited GRC Resources and Budget Constraints

Most mid-sized companies operate with lean GRC teams. Budget constraints hinder investment in fraud detection tools like user behavior analytics or real-time alert systems. According to ACFE’s 2024 study, over half of all fraud cases occur due to weak or overridden internal controls—a risk magnified in firms lacking dedicated compliance capacity.Most mid-sized companies operate with lean GRC teams. Budget constraints hinder investment in fraud detection tools like user behavior analytics or real-time alert systems. According to ACFE’s 2024 study, over half of all fraud cases occur due to weak or overridden internal controls—a risk magnified in firms lacking dedicated compliance capacity.

Blind Trust in Long-Serving Employees

Familiarity breeds complacency. Many insider incidents involve staff considered loyal or beyond suspicion. The Ponemon Institute found that 1 in 5 insider frauds involved “trusted” employees exploiting privileged access. When firms equate tenure with integrity, they often ignore the need for independent oversight or segregation of duties, leaving room for misconduct.

Compliance Gaps in Listed Mid-Caps

Being publicly listed doesn’t guarantee governance maturity. Many mid-cap firms face regulatory obligations without scaled internal systems to meet them. A 2024 survey showed 55% of listed mid-sized firms lacked robust compliance frameworks, increasing exposure to fraud, conflicts of interest, and enforcement risks.

Neglect of Insider Behavior Monitoring

While external threats like cyberattacks, audits, and investor scrutiny often dominate risk discussions, internal behavior in mid-sized firms remains largely unmonitored. A 2024 report found that while insiders were involved in 60% of data breaches, only 25% of companies regularly monitor user activity. This oversight gap allows repeated privilege abuse or policy violations to slip through undetected.

Cultural Resistance to Monitoring Tools

Employee pushback is common when firms try to implement tracking tools. In trust-driven environments, monitoring feels intrusive and misaligned with the culture. A recent survey revealed that 63% of employees would consider leaving their company if strict monitoring measures were put in place. This resistance slows adoption of essential controls like access logging or behavioral alerts.

Overlapping Roles and Conflicts of Interest

In mid-sized setups, employees often wear multiple hats, including approving vendors, processing payments, and handling reconciliations. This lack of segregation weakens internal checks. ACFE reports that 42% of frauds stem from the absence or override of internal controls, such as dual approval or independent reviews.

Manual Workflows and Silent Fraud

Email-based processes, spreadsheet approvals, and informal reimbursements create room for “quiet” fraud. Without automated alerts or audit trails, misconduct can persist unnoticed. A 2025 Bloomberg case revealed how a mid-sized retailer lost$1.8 million over two years through undetected expense fraud, highlighting the cost of informal systems.

Regulatory Burden Without Execution Support

Compliance demands are growing, but mid-sized firms often lack the structure to execute. From data protection to ESG, obligations now rival those of large enterprises, without matching resources. The U.S. Chamber of Commerce noted in 2024 that 51% of small and mid-sized businesses see regulation as a key operational burden.

Overreliance on Financial Audits

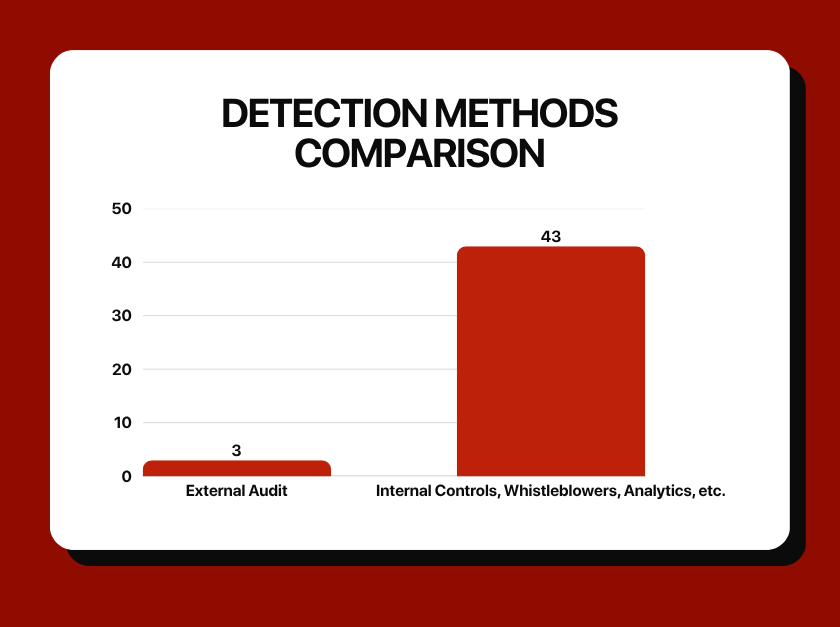

Annual audits offer false comfort. ACFE data shows external auditors detect only 3% of fraud cases. Behavioral misconduct like override abuse or insider collusion rarely shows up in financial statements. Without internal controls focused on behavior, red flags remain buried in day-to-day operations.

Mitigating Insider Risk

Mid-sized firms often walk a tightrope between agility and oversight. With lean GRC teams, fast-moving operations, and high dependence on trust, insider risk becomes a quiet but potent threat, often surfacing only after the damage is done. Fortunately, leading companies are showing how risk exposure can be materially reduced through deliberate, scalable steps:

- Build Professional Skepticism Across Vulnerable Functions The absence of healthy doubt is a core enabler of internal fraud. Teams often trust colleagues or assume “it must have been reviewed.” Embedding professional skepticism via training, risk orientation, and scenario-based workshops can shift the mindset from “compliance” to “risk management.” For example, a Southeast Asian mid-cap embedded a red-flag checklist in monthly reviews, flagging odd vendor payment cycles, duplicate invoices, and large round-number payments, unearthing a 3-year-old ghost vendor scheme.

- Layer Forensic Thinking Into Control Design Traditional controls (approvals, reconciliations) often lack the forensic intent to catch manipulation. Mid-sized firms should embed anti-fraud thinking into finance and procurement workflows, e.g., flagging new vendors created by the same user who approves invoices, or detecting payment splits just below approval thresholds. In one Indian mid-cap, forensic review of vendor master data found multiple entries linked to a single PAN number, leading to the unravelling of a procurement kickback loop.

- Regular Rotation of Duties in Sensitive Functions Fraud schemes often rely on a single insider managing a process end-to-end. Periodic job rotations, especially in roles like vendor onboarding, payroll processing, or loan disbursements, introduce fresh eyes and reduce opportunity. This approach helped a fintech firm in India detect a backdated disbursement manipulation after a temporary replacement questioned an old approval trail.

- Maintain an Always-On Fraud Ledger Beyond incident response, firms should maintain a fraud event registry tracking red flags, near misses, overrides, and ethical hotline tips, even if they don’t lead to confirmed fraud. Patterns often emerge when seen over time. One APAC manufacturer built such a ledger, which helped internal audit connect repeated override incidents across multiple geographies, ultimately leading to the identification of a multi-country expense fraud ring.

- Use Analytics to Spot What Human Eyes Miss User Behavior Analytics (UBA) and Data Loss Prevention (DLP) tools help surface subtle anomalies—after-hours logins, file transfers, unusual access routes—that are easy to miss otherwise. A Pune-based fintech used behavioral analytics to flag an employee repeatedly sending encrypted files to a personal account. The employee claimed it was for “offsite backup,” but further investigation revealed attempted IP theft. Behavioral AI can flag anomalies across cloud apps, VPNs, endpoints, and collaboration tools. Analysts report time savings of up to 70% during investigations when AI assistants triage alerts and surface contextual patterns.

- Treat Culture as a Control Layer Controls fail silently when employees are conditioned to ignore red flags or assume silence is safer. Embedding ethical tone through leadership modeling, anonymous reporting channels, and regular training creates cultural antibodies. In one APAC energy firm, a junior procurement executive flagged a vendor relationship via an anonymous whistle-blower tool, leading to the early unravelling of a collusion ring that had persisted for over a year.

- Secure Offboarding as if Breach is Guaranteed Exit events are when many insider incidents peak. Integrating HRIS and IAM systems ensures that resignations or terminations trigger immediate access revocation. Tesla’s 2023 incident, where former employees leaked sensitive data after their departure, is a case in point. A Southeast Asian R&D firm avoided similar fallout by enforcing just-in-time provisioning and de-provisioning protocols linked to HR workflows.

- Have an Insider-Specific Response Playbook Most companies have IR plans, but few have tailored playbooks for insider threats, which are often more subtle and reputationally sensitive than external attacks. One U.S. retailer that received a tip-off of employee theft initiated an internal investigation within 48 hours, preserving digital forensics, locking access, and launching containment discreetly. The firm suffered minimal reputational damage, unlike a peer that took weeks to act and landed in the media.

- Audit What You Assume Is Working Internal audit/assurance functions should be empowered to do anomaly-led investigations, e.g., looking for outlier spend patterns, non-business hour approvals, or repeated manual journal entries just before quarter close. Even one such “audit sprint” per quarter can raise deterrence significantly and align IA more closely with forensic objectives.

- Run Integrity Checks on Third Parties and Employees Collusion risk is highest in procurement, sales, and distribution. Instituting continuous third-party screening, conflict-of-interest disclosures, and employee lifestyle audits (especially in high-risk roles) helps detect early signs. One Indian mid-cap FMCG firm used a third-party integrity check and found that a key distributor was also a silent partner in a logistics vendor, triggering reallocation of contracts.

Conclusion: Don’t Underestimate the Enemy Within

Insider risk is often under-discussed in boardrooms, overshadowed by flashier external threats. Recent cases from banks in India to factories in America demonstrate that misuse of trust and collusion are alive and well in 2024-25, costing businesses dearly. As companies push for growth, they must ensure not to fall into the trap of assuming “it can’t happen here.”

The truth is that as organizations grow, so do the opportunities for insiders to exploit gaps, especially if controls and culture don’t keep up.

The encouraging news is that many insider risks are manageable with foresight and vigilance. By learning from studies like the ACFE’s annual report and industry surveys, companies can understand where they are most exposed. For example, knowing that operations, accounting, and sales departments account for a large portion of internal fraud cases can prompt targeted control improvements in those areas.

Recognizing that collusion multiplies damage fourfold should spur better cross-checks and rotation in high-risk functions. And remembering that employees are often the heroes in detecting fraud emphasizes the value of a speak-up culture and employee training.

Ultimately, effective insider risk management is a balancing act: trust but verify. Companies should cultivate a high-trust workplace but verify that trust through robust controls and oversight. External defenses and cybersecurity matter, but they are not sufficient on their own. Internal vigilance is equally crucial.

In an era of advanced analytics and AI, businesses have powerful tools to monitor for anomalies; combined with human ethics and sound governance, these tools can tip the balance in favor of the honest majority. Mid-sized firms that embrace these principles will not only protect themselves from insider threats but also create a more transparent, accountable environment that investors, regulators, and employees themselves can have confidence in.

In the journey of growth, keeping an eye on the “enemy within” is now an essential part of sustaining success.

Infographic Sources; https://www.acfe.com/report-to-the-nations/2024/, https://www.proofpoint.com/us/resources/threat-reports/ponemon-cost-of-insider-threats, https://www.ey.com/en_gl/forensic-integrity-services/global-integrity-report-2023, https://www.acfe.com/report-to-the-nations/2024/, https://hbr.org/2022/01/why-employees-dont-report-unethical-behavior, https://www.acfe.com/report-to-the-nations/2024/